As the Federal Reserve begins its series of rate hikes to control record-high inflation, investors need to be aware of which real estate segments may face challenges in the foreseeable future. Real estate offers investors long-term stable income, protection from inflation, and diversification benefits due to its low correlation with other asset classes.

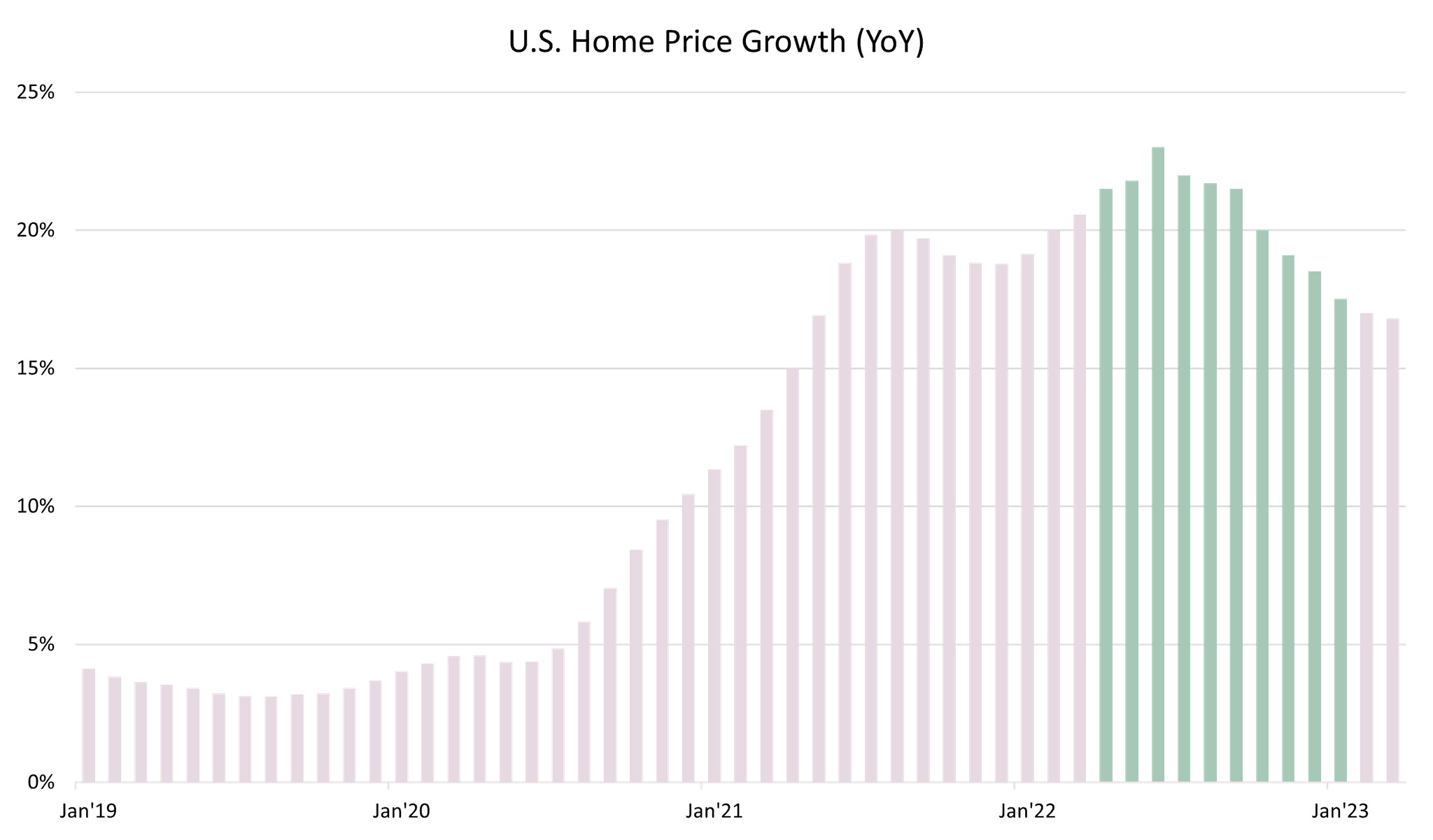

Home values across the U.S. have hit record levels in 2021, in many instances with prices skyrocketing around $100,000 vs. pre-Covid levels. The surge is happening with remote work flexibility tied with supply chain issues that crippled the construction of new homes.(1) According to Zillow researchers, U.S. home prices in March 2022 were up 18.8% from a year ago, forecasted to reach 22.0% by end of May with the acceleration in annual home price growth. For comparison, the largest 12-month uptick leading up to the 2008 housing crash was recorded at 14.1% only. Their latest forecast predicts a subtle slowdown in the annual growth rate by February 2023, reaching 17.8% which is still about four times greater than the average annual rate of home price growth recorded since 1986 (4.6%).(2)

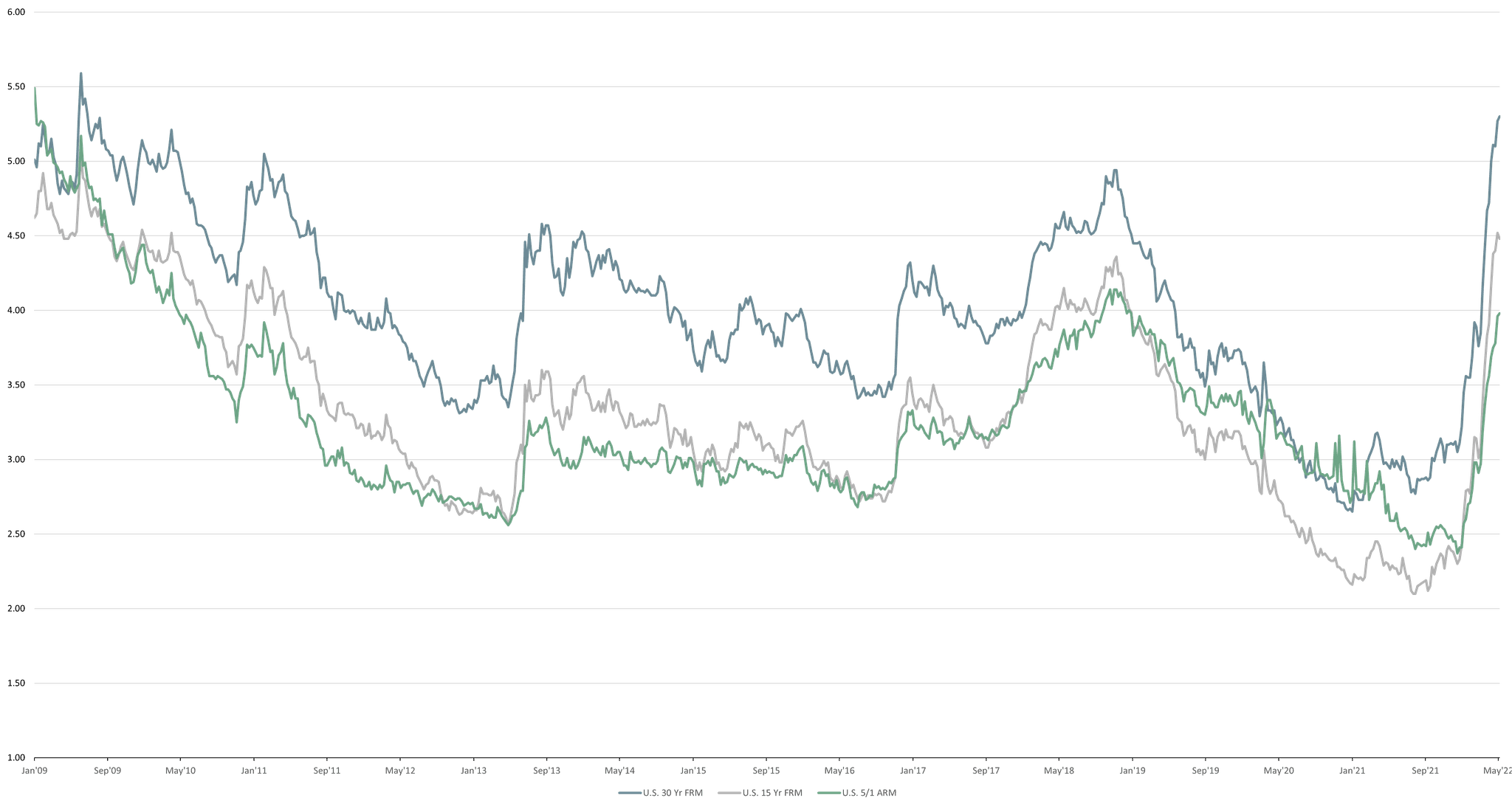

In its May FOMC meeting, the Federal Reserve announced its plan to move forward with a half percentage point rise in interest rates to control the record-high inflation. This move, the most aggressive since 2000, has widely affected mortgage rates, with the 30-year rate reaching ~5.3% in May 2022 - its highest level since 2009. Elevated mortgage rates coupled with four-decade high inflation, rising home prices, and lagging home construction have made homeownership less affordable, especially for first-time buyers. This could delay home purchases for millennials looking to upsize, who may instead opt for single-family or one-/two-bedroom apartment rentals.

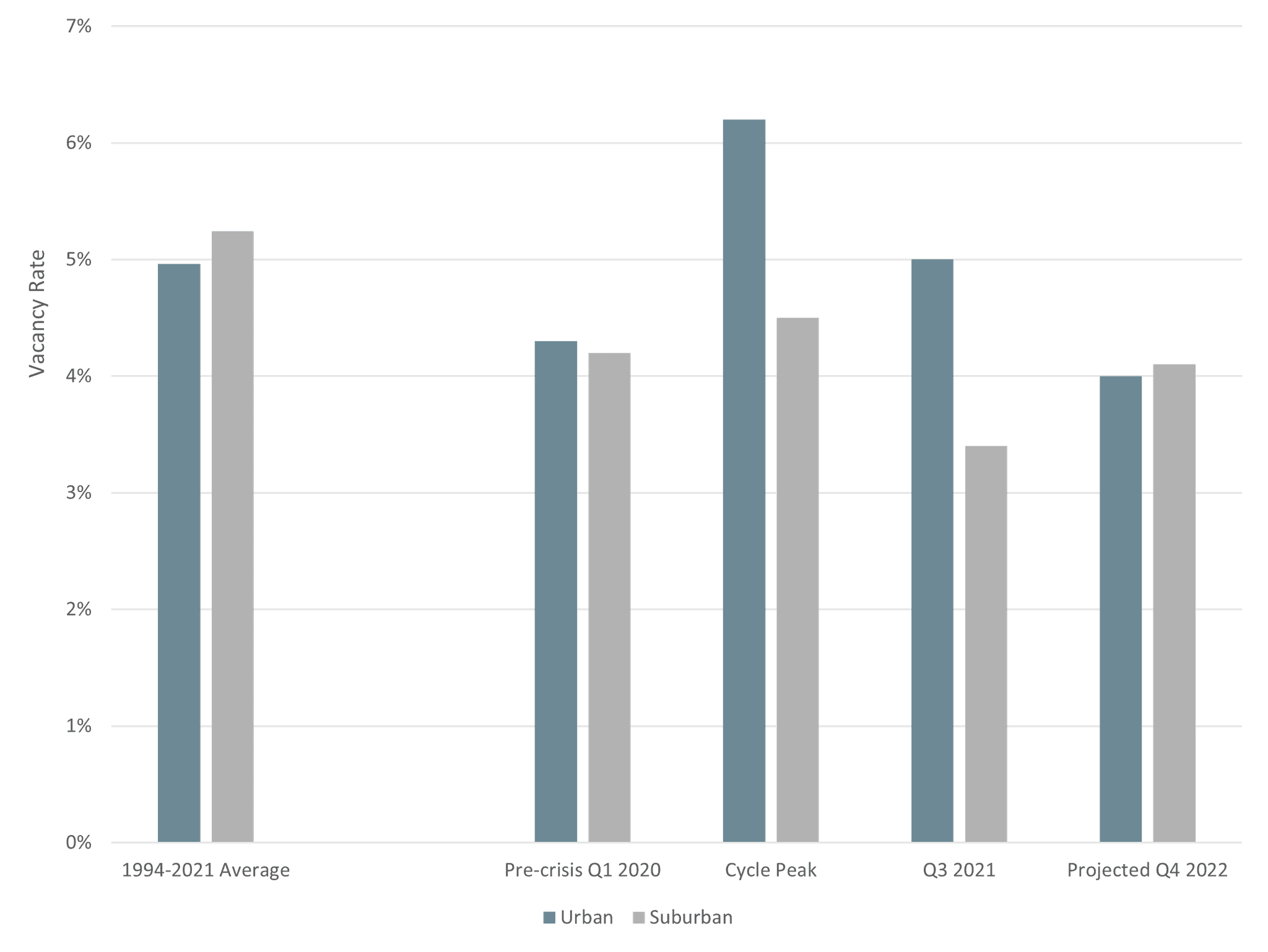

Multifamily assets have remained resilient throughout the pandemic and experienced a record-breaking year in 2021. The sector set an annual absorption record of 617,500 units in 2021, with overall vacancy rates falling 2.2% compared to the year earlier, and net effective rents increased 13.4% over the same period.(3) Strong multifamily fundamentals have persisted even through Q1 2022 due to favorable migration trends, high household formation, and strong wage and job growth - all of which contributed to the continued demand.

Outlook

The multifamily sector is set for an unparalleled year ahead, with increased household formation and the return of workers to offices driving multifamily properties in urban areas to fill up vacant spaces. Urban areas experienced an average vacancy rate increase of ~2% during the peak of the pandemic. According to a recent CBRE report, vacancy rates are forecasted to fall to 4% by the end of 2022.(4)

II. The Office Market

Outlook

The U.S. office market activity strengthened in the second half of 2021 and the momentum would likely be sustained throughout 2022 by strong job growth and demand for Grade A office space. The conversion of low-grade office buildings to warehouses is also becoming more popular to accommodate the rise in demand for industrial space driven by the e-commerce boom across the country.

As high-quality office assets are prioritized to retain and attract workers, more landlords of low-grade office buildings are opting for the conversion path.

III. Single-Family Rental Market

The Single-Family Rental (SFR) space has strong fundamentals, mainly driven by the millennial generation aging into prime family formation years, high cost of ownership, and supply that has constantly lagged new household formation. This segment is seen as an arising opportunity as the Fed continues to raise rates that push mortgages to record highs, making homeownership for first-time buyers unaffordable and consequently forcing them into the rental space. Green Street's analysis suggests that although mortgage rates remain low relative to the long-term history (back to levels seen in 2018), it is the speed and magnitude of the change in rates coupled with significant cumulative home price appreciation that leave homebuyers with much higher debt service loads seen in the market over recent years.

Outlook

SFR fundamentals could benefit most directly from the recent rise in homeownership costs. In the near term, the limited inventory of affordable single-family homes (both for rent and for sale) may experience further reductions. This is due to existing SFR tenants being forced to stay in place for longer periods to save on down payments. In addition, a growing number of prospective homebuyers are “trading down”, which will take up rental inventory off the market.

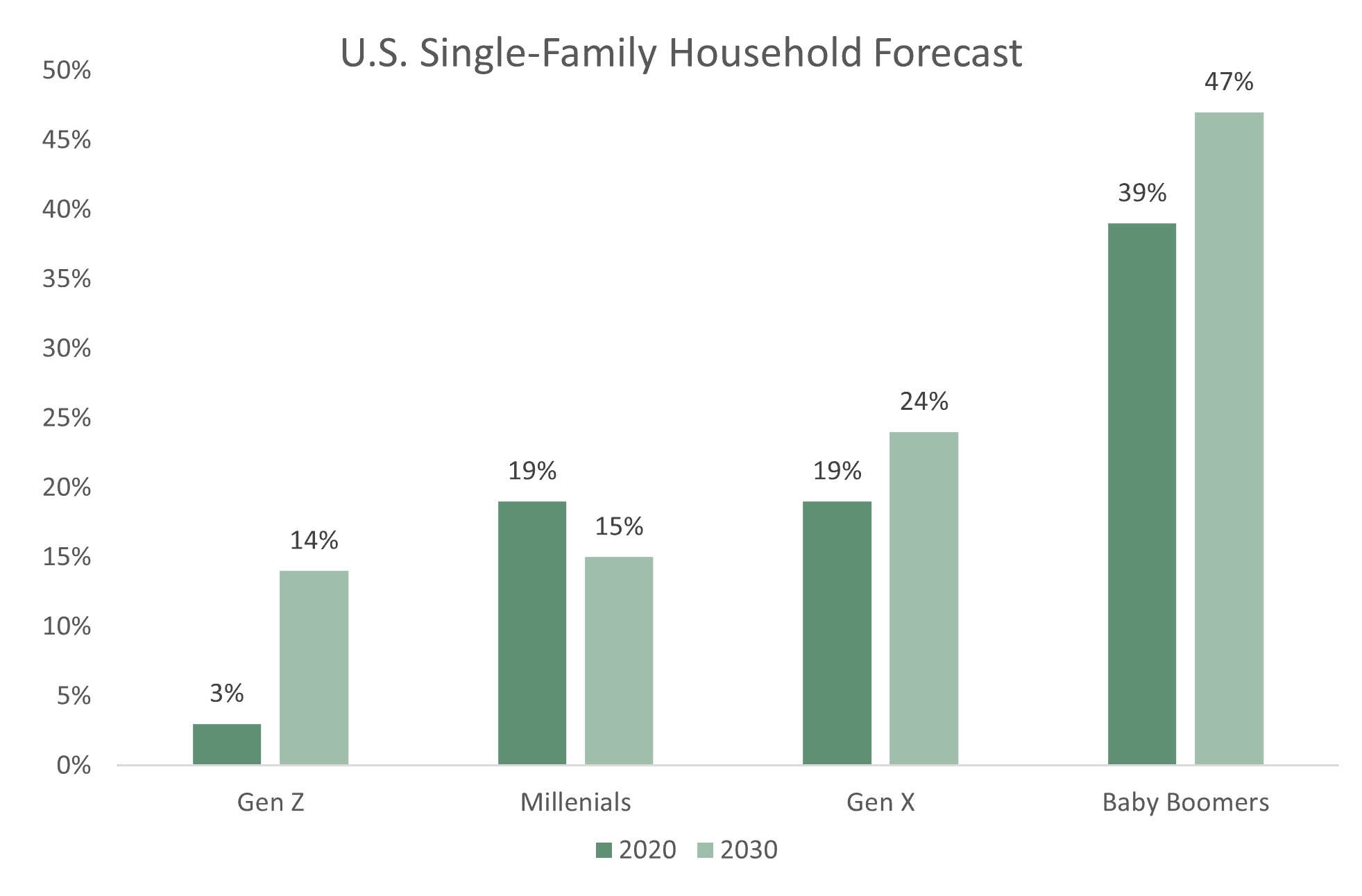

The space is experiencing strong demand primarily by aging millennials looking to move into bigger spaces to grow families. Freddie Mac forecasts that sole-person households are expected to increase from 36.1 million to 41.2 million by 2030,(5) and millennials are not the sole cohort to participate in this rise.

Petiole grew its expertise in private real estate through many cycles of investing in this asset class. We maintain a disciplined approach in deal selection, risk management, and portfolio construction. Contact our team to know our real estate strategy in the U.S. and key regions.

References:

Investing in Real Estate During Covid?, Alison Cenname, JP Morgan, 15 March 2022

Zillow February 2022-February 2023 Home Value & Sale Forecast, Zillow, 16 March 2022

U.S. Multifamily Cap Rate Report, CBRE powered by Valuation VIEW, Q4 2021

U.S. Real Estate Market Outlook 2022, CBRE, 8 December 2021

The Growth of Sole-person Households: Creating Even More Demand for Smaller, More Affordable Homes, S. Khater, L. Kiefer, A. Atreya, Freddie Mac, 26 August 2021