As the Federal Reserve ditches the term "transitory" and turns more hawkish, private debt has been brought into the spotlight. What value can this asset class play in a portfolio?

Introducing: Private Debt

What is Private Debt?

Private debt, or private credit, is an advancement of capital to a private borrower who has obligations to make interest payments on the borrowed sum and repay the principal capital back at a predetermined maturity period. It can be classified into direct lending, mezzanine debt, distressed debt, special situation debt, and venture debt.

The debt is usually secured and has ample protections/covenants in place. Furthermore, the debt is also tailored to the requirements of the borrower, making it relatively illiquid when compared to public market debt.

Private debt’s growth in popularity consequently led to its global AUM increase by more than 4 folds over the past decade.

The Borrowers

The borrowers in the private debt market tend to be small & medium-sized enterprises, having an EBITDA in the range of $3-100 million, the many of them go into the private debt market without a public credit rating.

When companies have liquidity needs and don’t have access to the public capital markets, private lenders would step in quickly with amendments. During the first wave of the COVID crisis in 2020, many private lenders helped companies that were at risk of breaching financial maintenance covenants, solidifying private debt's reputation as “bear market capital” - available in times of turmoil but at a price.

The Lenders

The lenders are asset or investment managers through multiple lending vehicles, i.e. BDCs, private debt funds, CLOs, or mutual funds. Private debt funds historically targeted institutional investors, but a growing number of asset managers are now expanding to accredited individual investors.

Private Debt vs High Yield

Private debt offers several advantages over its public market counterpart (High Yield), such as floating rate, lower volatility, stronger covenants, and better monitoring rights. This comes, however, at lower liquidity and the need for a more resource-intensive due diligence process.

Borrower Perspective

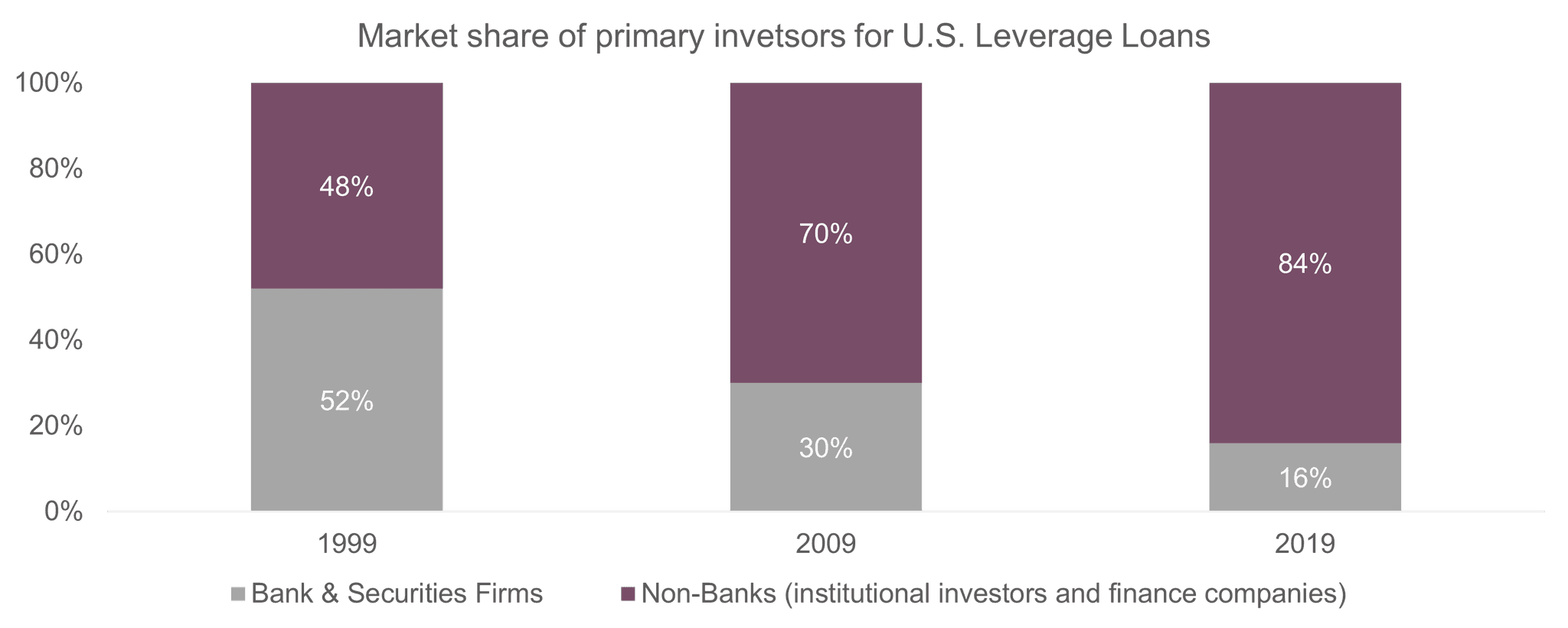

The demand for private debt has grown since the global financial crisis of 2008 as banks reduced their lending activity to small- and medium-sized enterprises. As an aftermath of the global financial crisis, a series of new regulations, such as Basel III and Basel IV, required banks to increase their capital basis, tighten underwriting standards, and generally enhance reporting. This drove banks to become more risk-averse, shrinking their balance sheets and narrowing their lending products as they struggled to make money.

The past decade has been characterized by low-interest rates; people were looking for yield outside the traditional fixed income asset class. A conservatively managed, well-diversified private debt portfolio offered investors a viable alternative to fixed income. Private debt has become more and more attractive to investors for several reasons:

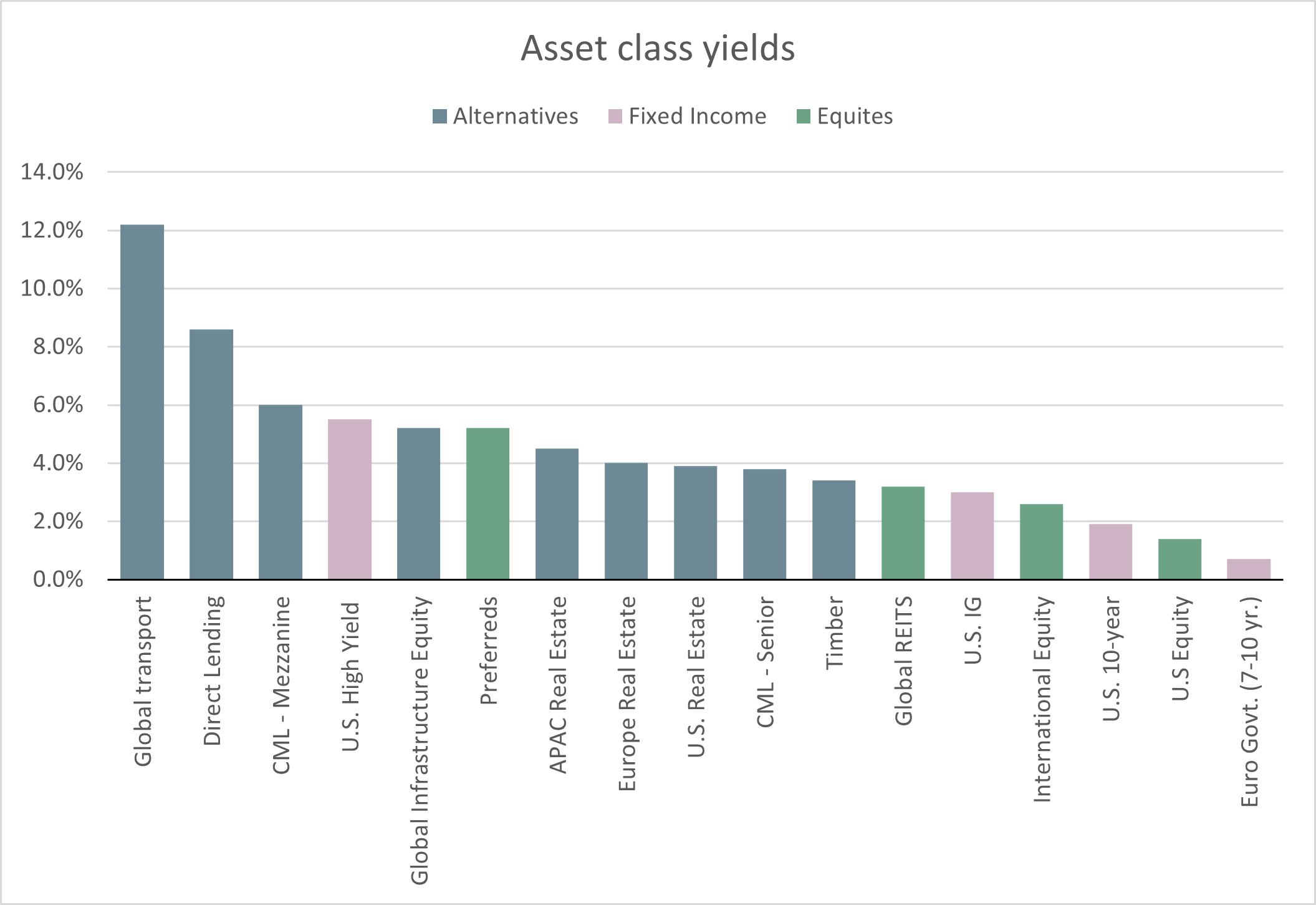

Attractive Risk/Reward - Investors in private debt receive a return/yield premium over traditional fixed income assets. This excess return is often referred to as an “illiquidity premium” and is primarily driven by the complexity involved in originating, underwriting, structuring, and exiting private debt investments.

Diversification Benefits - Private debt can offer exposure to a wide range of sectors, such as real estate, infrastructure, or corporate financing.

Better Recovery Values - Around 95% of bonds issued on the public market are unsecured, i.e. not backed by assets that can be sold in case of default. By contrast, private debt is often secured, thus reducing the risk for investors. Recovery values for private debt are generally much higher than those of the public market (private corporate debt has a recovery value of around 80% compared to 50% for an unsecured public corporate bond).

Private Debt in a Rising Rate Environment

Persistent supply chain issues, China's Zero COVID policy, pent-up consumer demand, and commodity price swings on the back of the Russo-Ukrainian conflict have injected huge inflationary pressures that the U.S. Federal Reserve adopted a more hawkish stance to contain these pressures.

The squeeze on traditional fixed income is unlikely to abate, which positions private debt as a valuable component in a portfolio due to its resilience against rising rates and inflation.

Floating Rate Loans - In a rising rate environment, floating rate loans are highly attractive as income can rise along with interest rates. Private debt usually has a floating rate which limits both interest rate and duration risks that are inherent to public fixed income.

Flexible Deals - Since private debt is often a result of direct negotiations between the lender and the borrower, the managers/lenders can generally negotiate better protections, e.g. call protections, covenants, etc., making the asset class more defensive in such a volatile environment.

Less Volatility - Private debt has been experiencing less volatility as it is not traded on public markets and because valuations are generally based on the fundamentals of borrowing companies, allowing private loans to offer attractive returns.

Conclusion

The private debt market still has considerable room to grow, and more investors are anticipated to continue allocating to private debt strategies for their unique characteristics.

As part of Petiole's diversified private market investment programs, we have been harnessing private debt's potential over the past years.

Contact our expert team today to find out more about how private debt can be valuable to your investment requirements.

References:

Five trends in private debt for 2021 and beyond, Vistra Insights, 31 March 2021

The Rise of Private Markets: Secular Trends in Non-Bank Lending and Their Economic Implications, Ares Capital, February 2020

Private Debt Investing: Benefits & Current Market Conditions, Saratoga Investment Corporation

Private Debt in an Institutional Portfolio, Sanjay Mistry & Tobias Ripka for Mercer Private Markets, CAIA Association, Q4 2017

Public versus private debt – what’s the difference?, Marianne Zangerl, MARIANNE ZANGERL, abrdn.com, 11 December 2019

Private Debt: The Rise of an Asset Class, Alan Flanagan and Robert Wagstaff, BNY Mellon

Private Credit’s Rapid Growth: A Secular Trend, Blackstone, April 2022

Guide to Alternatives – 1Q 2022, D. Lebovitz, M. Pandit, N. Vyas, JP Morgan Asset Management, 28 February 2022

Private Debt: A Lesser-Known Corner Of Finance Finds The Spotlight, E. Gunter, A. Latour, J. Maguire, S&P Global, 12 October 2021