Risk Culture in Decision Making

Although risk in private markets is often perceived as higher than in public markets, alternative investments present potential for higher returns, portfolio diversification benefits, and resilience throughout recession periods. A customized risk framework could help in achieving sound and well-informed investment decisions in private markets.

Risk Management in Public and Private Markets

In recent years, investor interest has increased in alternative asset classes as an option to diversify portfolios out from public markets. The market share of private investments has grown so significantly that it has become critical for portfolio managers and investors to: a) deeply understand the key risks that come with investing in alternatives, b) how they can be properly embedded and assessed in the decision making and ultimately mitigated, and c) how they compare against the public market risks. The typical risk categories for private and public are quite defined and standardized. However, there is a substantial difference in the way those categories are interpreted and managed in private markets due to the nature of these investments. So what's the major challenge?

In both public and private markets, credit risk is defined as the loss of assets due to credit events of the issuer, but it is assessed and managed differently. In public markets, the credit quality of an issuer is usually provided by rating agencies and is publicly accessible. Whereas in private markets, the financial health of a company requires a deep dive analysis performed in-house or through third-party vendors, and the results could be potentially affected by information asymmetry.

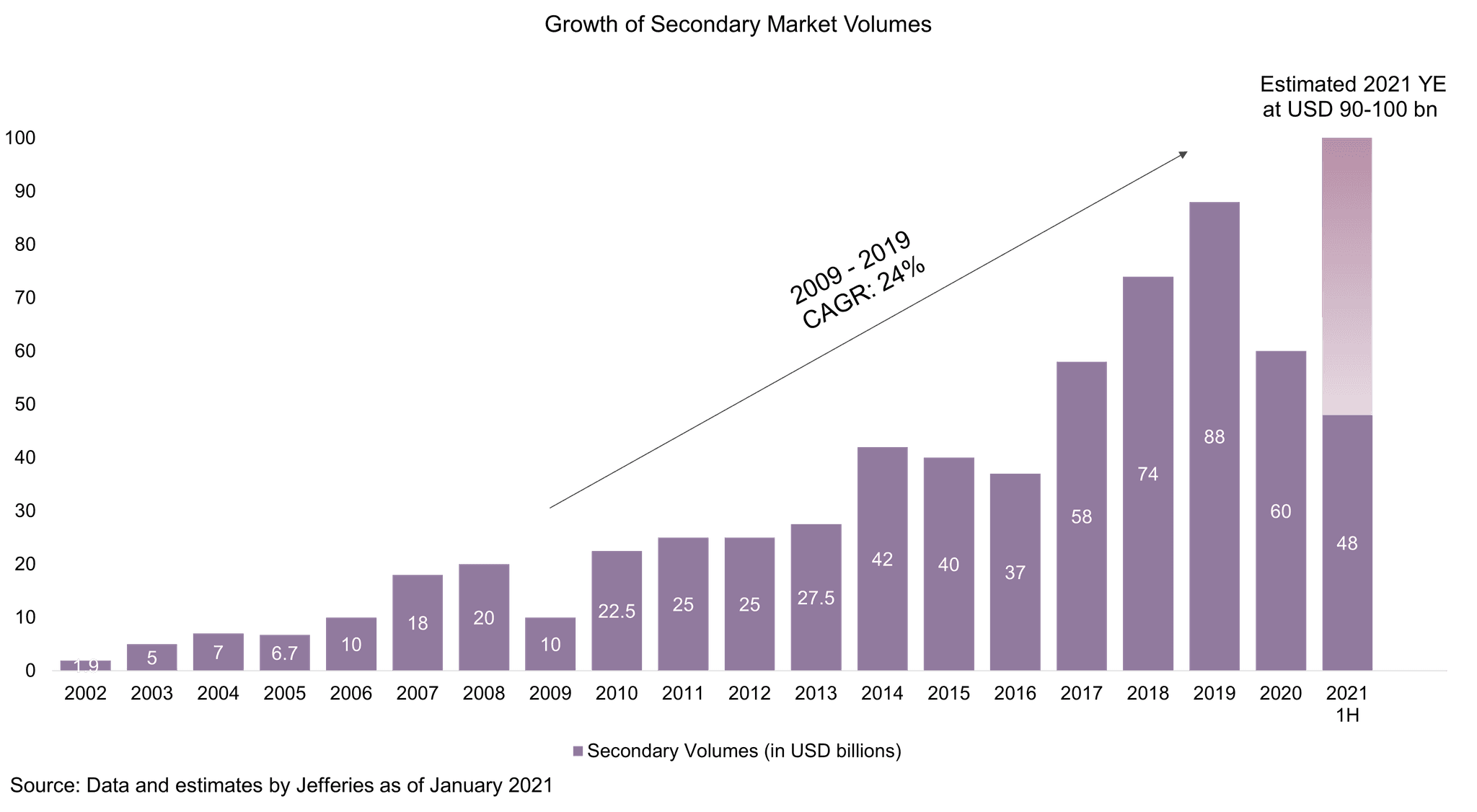

With liquidity risk, investment decisions are always impacted by the exit strategy and how easily the investments can be sold and converted into cash. In public markets, investors generally benefit from an efficient liquid market. For private markets, illiquidity might pose a drawback, i.e. investors do not have immediate market venues to sell the investment quickly. In the past few years, however, the secondary market volume has increased considerably from $18 billion in 2020 to $48 billion through the first half of 2021, providing a viable option of liquidity for private markets.

I. Key Challenges and Opportunities - Risk vs Return Perspectives

Opacity, longer investment horizons, and illiquidity - these are the main challenges inherent to the nature of private markets that risk managers face when building a risk framework for this asset class. On the other hand, the benefits of private markets include high returns, diversification, and resilience throughout recession periods.

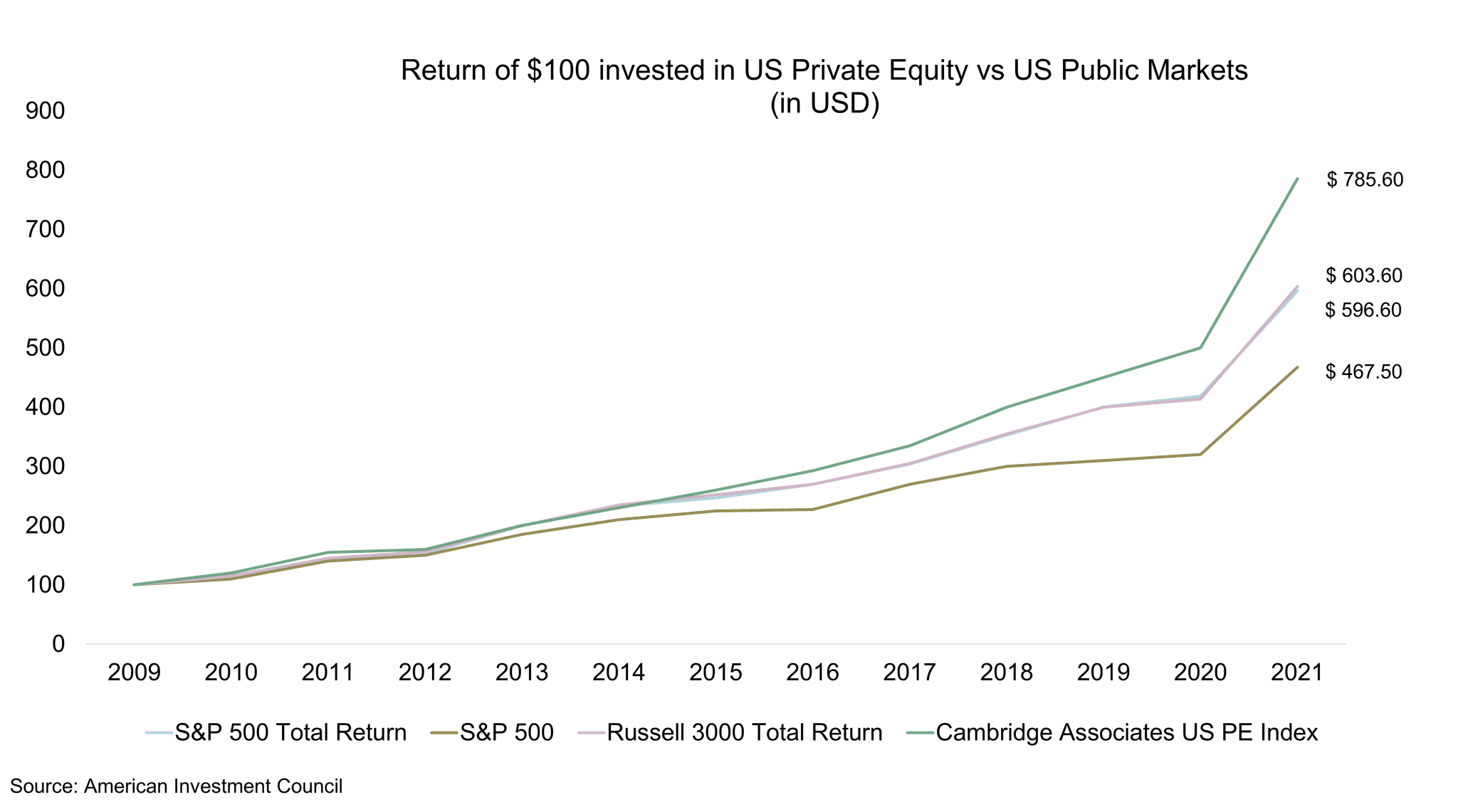

In a report by the American Investment Council, a $100-investment in U.S. private equity would have outperformed the same investment amount in U.S. public markets over the last 12 years. Note, though, that the benefits in the returns should always be considered alongside the investment risk perspective, as a meaningful and appropriate risk assessment can increase transparency and alignment with investors’ needs. The investment risk profile must be consistent with the investment strategy and the expected return profile.

A robust risk framework should always consider both systematic and idiosyncratic factors related to the investment. The extent and depth of analysis of these factors, and the data requirements underneath, mostly depend on using either a top-down or bottom-up approach; the former is more suitable for fund investments while the latter better applies specifically for co-investments and direct investments.

In a typical private equity co-investment, the critical systematic factors stem from the general market conditions and performance which ultimately impact the deal valuation, supply and demand dynamics, the cyclicality of the sector, and any potential sensitivity to other macro drivers like inflation and interest rates.

The idiosyncratic risk factors focus on the specifics of each transaction, both quantitative and qualitative. A risk framework should include an assessment of the target company's capital structure, the track record of the management in achieving budget and KPIs, financial health, and the exit strategy.

Case Study: A Private Equity Co-Investment

A well-structured bottom-up risk framework will support the decision-making process while constructing a private equity portfolio. The risk modeling should follow a holistic approach, whereby risk managers should not only identify and analyze the most crucial risks during the pre-acquisition phase but also define proper risk monitoring indicators to track the investment performance during the holding period.

Prior to the acquisition, one of the critical risks associated with a private equity investment is the company’s business risk. An analysis should be implemented around the company’s products and business lines, as well as the way the organization has been transformed within the years since its inception. This assessment is paramount to understand its market share, growth strategy, and future developments.

An equally important risk indicator is the company’s profitability - its performance and the management team's capabilities in executing business plans.

A deep dive analysis must be implemented around the company’s competitive landscape vs the market conditions, i.e. what are the key differentiators of the target company over its peers.

From a post-acquisition perspective, the most crucial monitoring indicators for a private equity investment are its financial health and the value creation levers.

A proactive, instead of reactive, approach to risk monitoring is vital. Setting up a solid post-trade risk monitoring checklist will help identify potential red flags associated with the company’s actual and expected performance, which are not yet embedded in the valuation and can be managed effectively in due time.

Petiole applies a disciplined approach to investing where we value long-term focus, thoughtful deal selection, and prudent risk management. Contact our expert team to learn more about how we construct private market portfolios.

References:

Risk in Private Equity Dr. Christian Diller, Dr. Christoph Jäckel, Montana Capital Partners

New Strategies for Risk Management in Private Equity, Capital Dynamics

EVCA Risk Measurement Guidelines, Investeurope, January 2013

Performance Update, American Investment Council, Q2 2021

Secondaries 2021 – A Buyers’ Market, Commonfound, November 18, 2021