Over the past decade, private credit providers have quietly increased their market share with borrowers forced to seek alternatives to traditional bank lenders. As COVID-19 continues to exacerbate corporate financial duress globally, tighter lending terms from traditional lenders and a reduction in active players in the market indicate significant future opportunities for private debt lenders.

USA

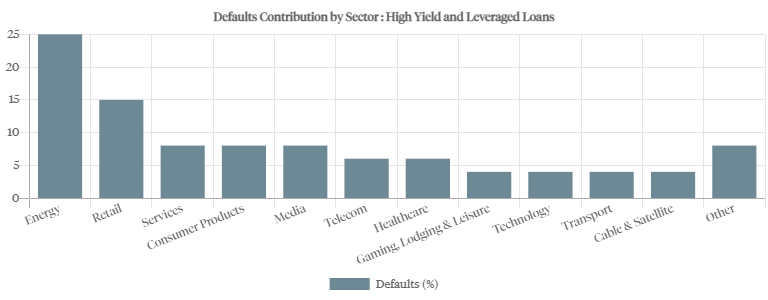

Although US leveraged loan defaults spiked in July 2020 to levels not seen since 2015, default rates remain comfortably below the Global Financial Crisis peak of 10.8% in November 2009. Some industries have been hit worse than others, with energy sector the largest contributor to defaults since the beginning of 2020 primarily due to bankruptcy filings from overleveraged drillers after the OPEC-Russia fallout.

"It’s important to note, though, that 75% of defaults across 2020 have been in industries other than energy; retail has been hit especially hard by the COVID-19 pandemic. Stabilization is expected heading into 2021 as vaccination programs start to take effect."

Europe

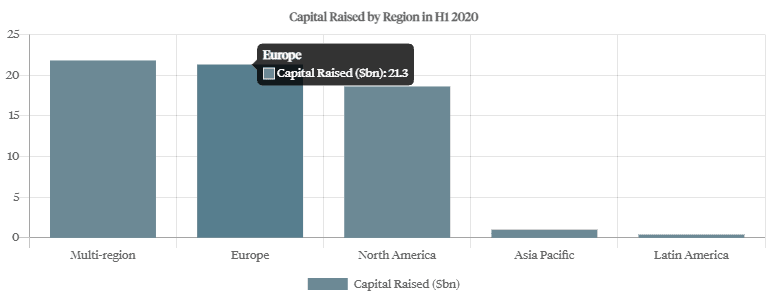

Overall conditions in Europe have also been buoyed by a stable and rapid governmental response to the pandemic. For the European private debt market, deal volume for H1 2020 was down 40% year on year. Interestingly, Europe has outraised North America in H1 despite this drop, while distressed debt dry powder remains a smaller percent of the market than in 2007.

Asia

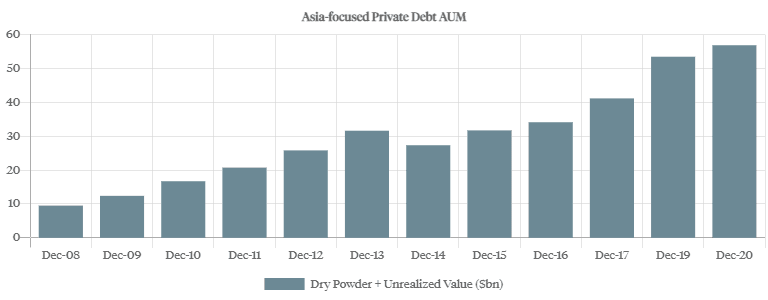

Economic recovery from the COVID-19 pandemic has been characterized by a sharp V-shaped rebound. Demand for private credit remains strong thanks to the reluctance of local banks to lend to mid-market corporates and the latter’s preference for the higher cost of debt over equity dilution.

Summary

"After a decade of mounting competitive pressures and borrower-friendly terms, the economic fallout from the global pandemic promises to create enticing opportunities in the private debt market."

Economic and structural terms have improved, with spreads increasing by 100-300 bps versus pre-COVID-19 pricing depending on leverage and credit, and covenants coming back in force. As a result, private debt offers investors attractive spreads versus traditional fixed income instruments and is now widely recognized as a powerful capital solution for mid-market companies going through rapid growth, a turnaround or acquisition that risk-averse banks are currently unwilling to provide. Competition has also reduced significantly across the private debt market lending space as general partners are turning their attention to liquidity issues within their portfolio companies.

Momentum remains particularly strong in the Asian private credit market thanks to the region’s swift handling of the COVID-19 pandemic. In Europe record dry power held by private equity funds is forecast to boost deal activity in 2021. The region outraised the US in H1 2020, indicating a market resilience which bodes well for future growth. We expect to see attractive opportunities in particular in secured second lien financing to middle market companies with strong equity cushions and opportunistic mezzanine financing in leveraged buyouts.