Global allocation to private credit has been gradually increasing due to its resilience against rising interest rates and inflation. Here you'll find out more about how this asset class is trending in Asia.

Why Private Credit in Asia?

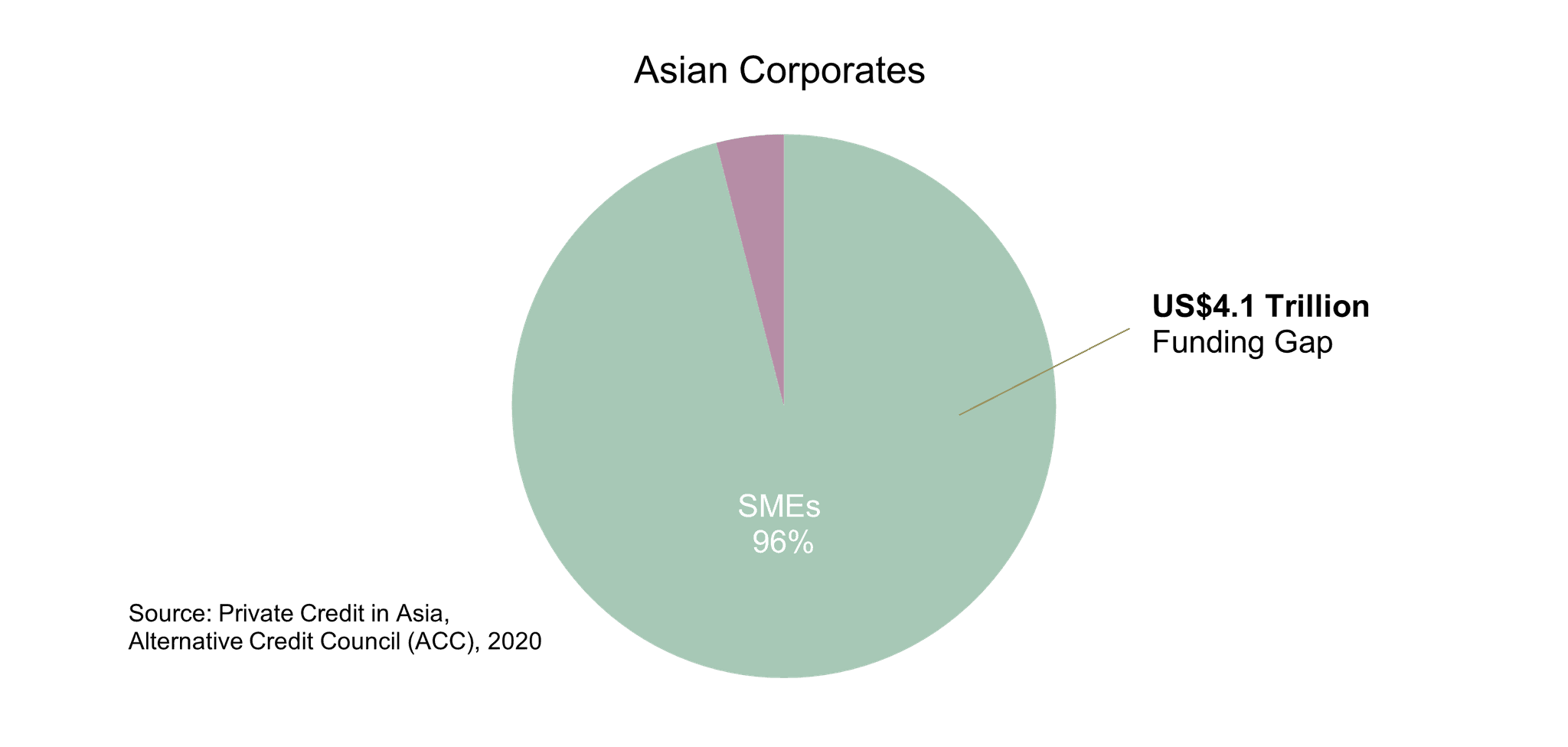

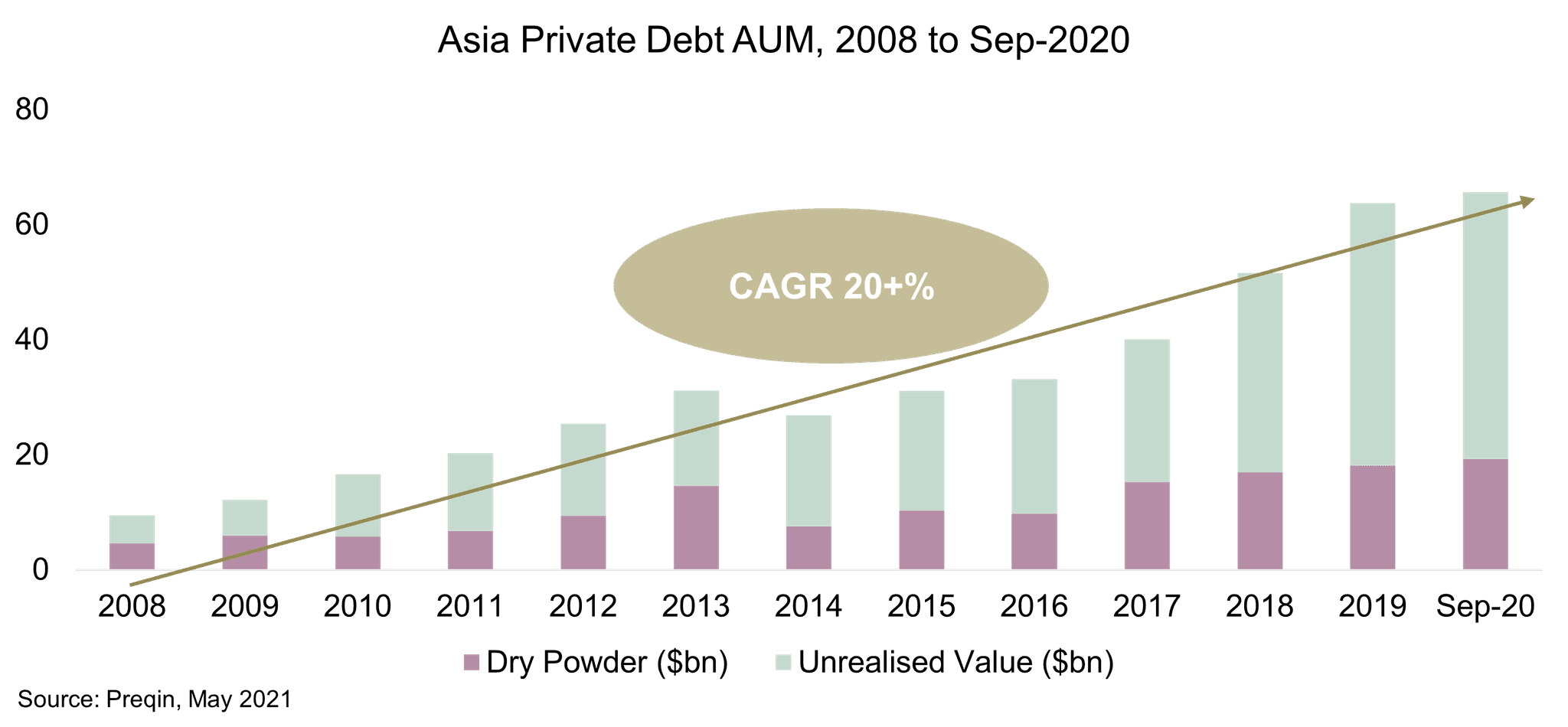

Since the outbreak of the pandemic, Asia remains the world's growth engine and with the gradual easing of travel restrictions in most of the region's economies, an increase in structural financing is observed.

Australia

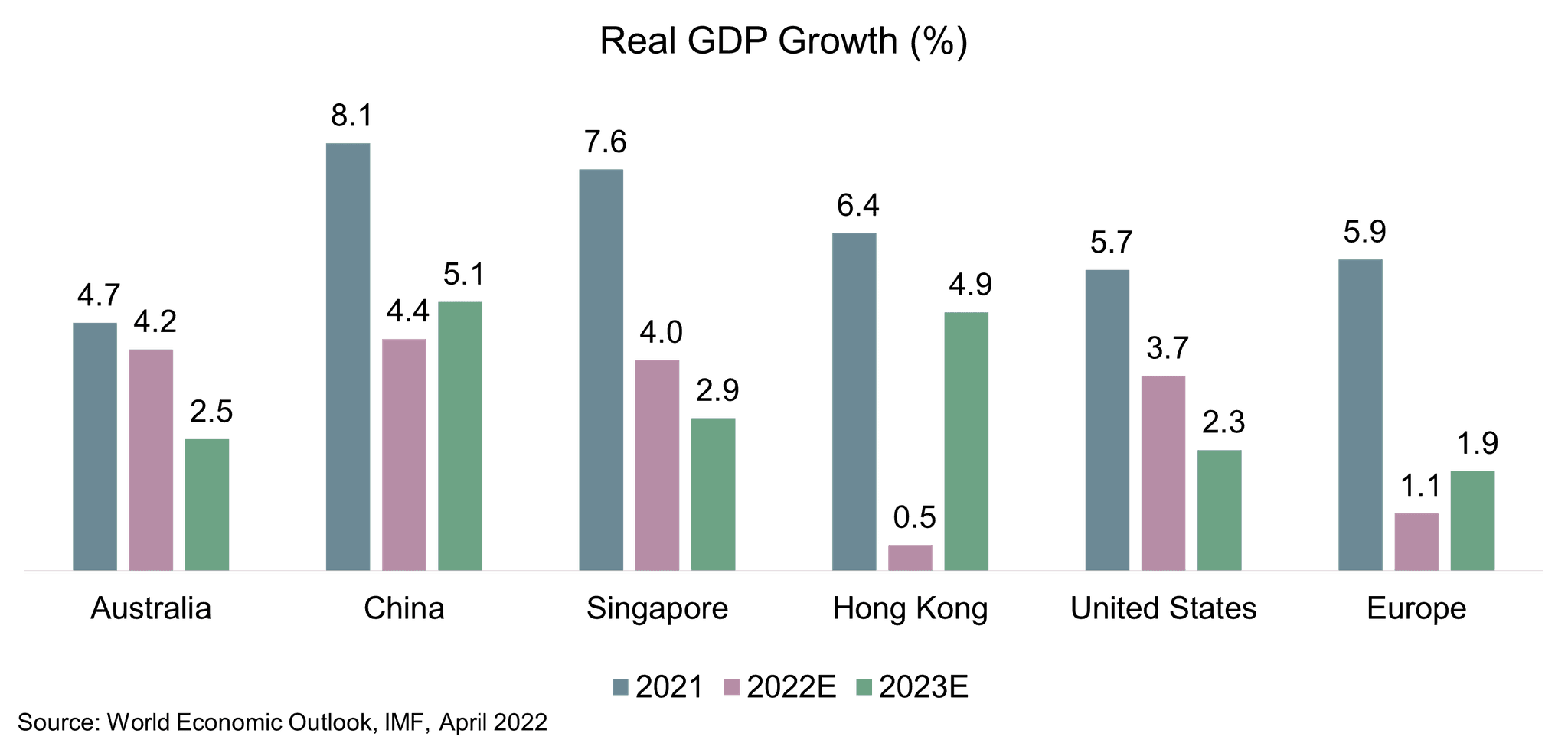

According to the IMF, Australia's economy will grow by 4.2% this year after recovering from the pandemic. Additionally, the economy is boosted by a low unemployment rate in 50 years, high consumer sentiment, and strong corporate performance.

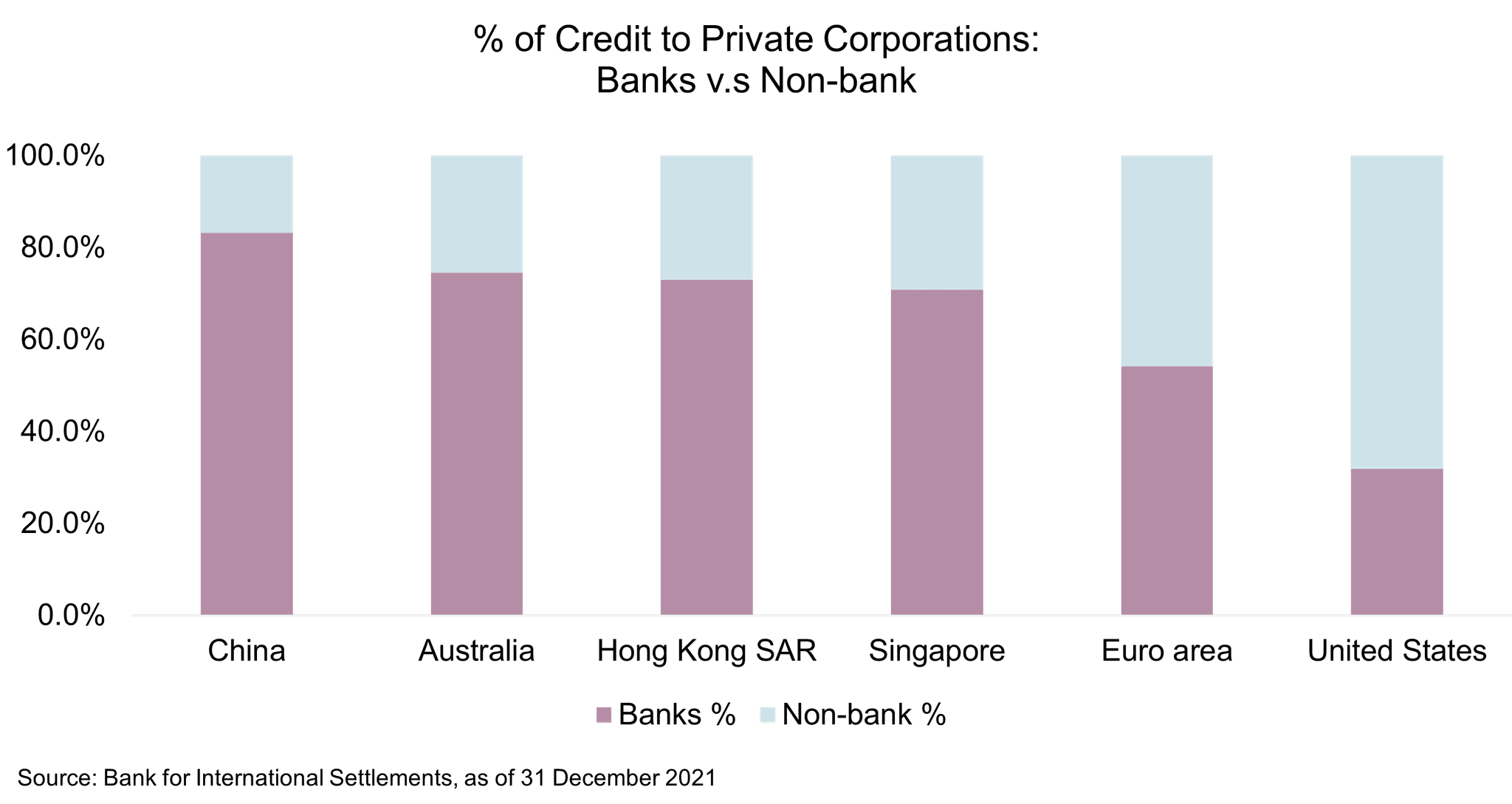

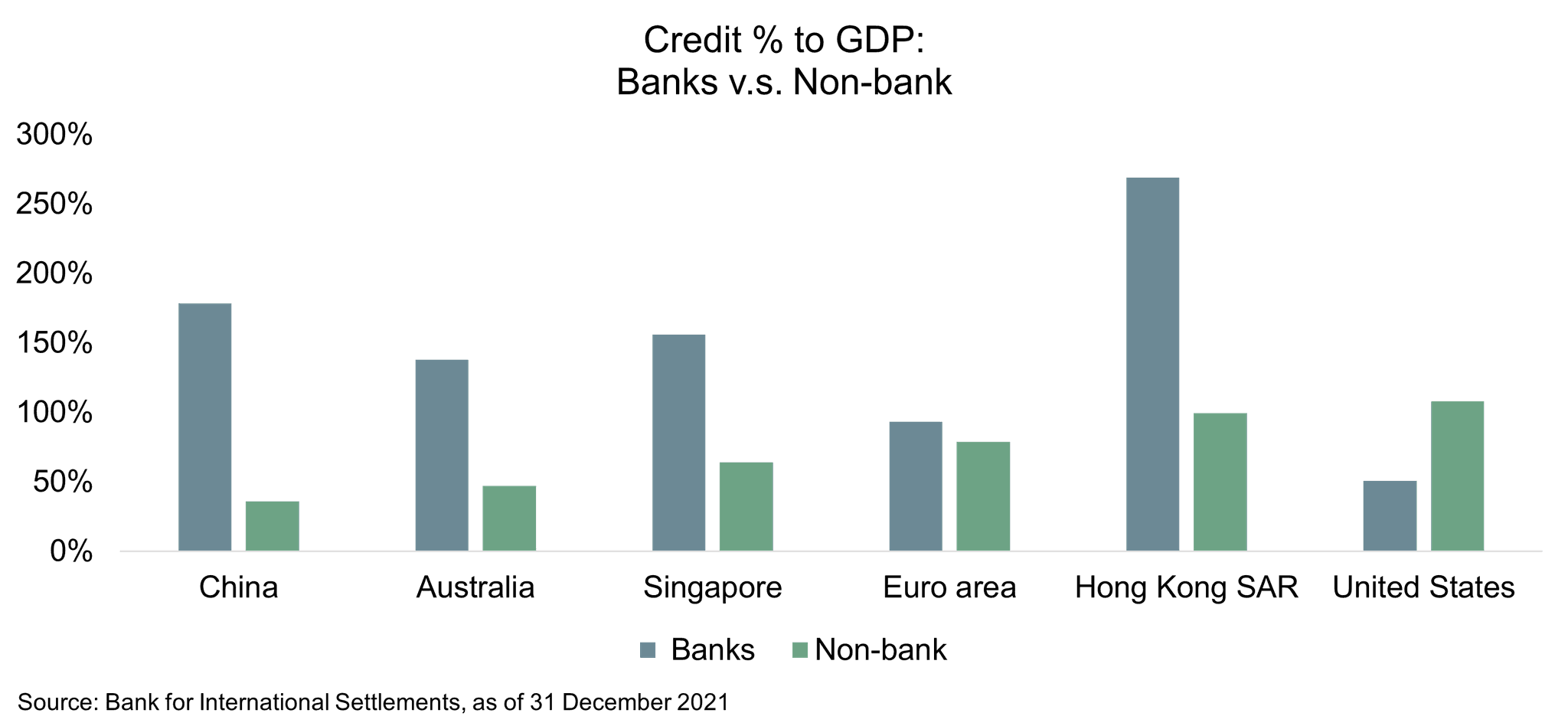

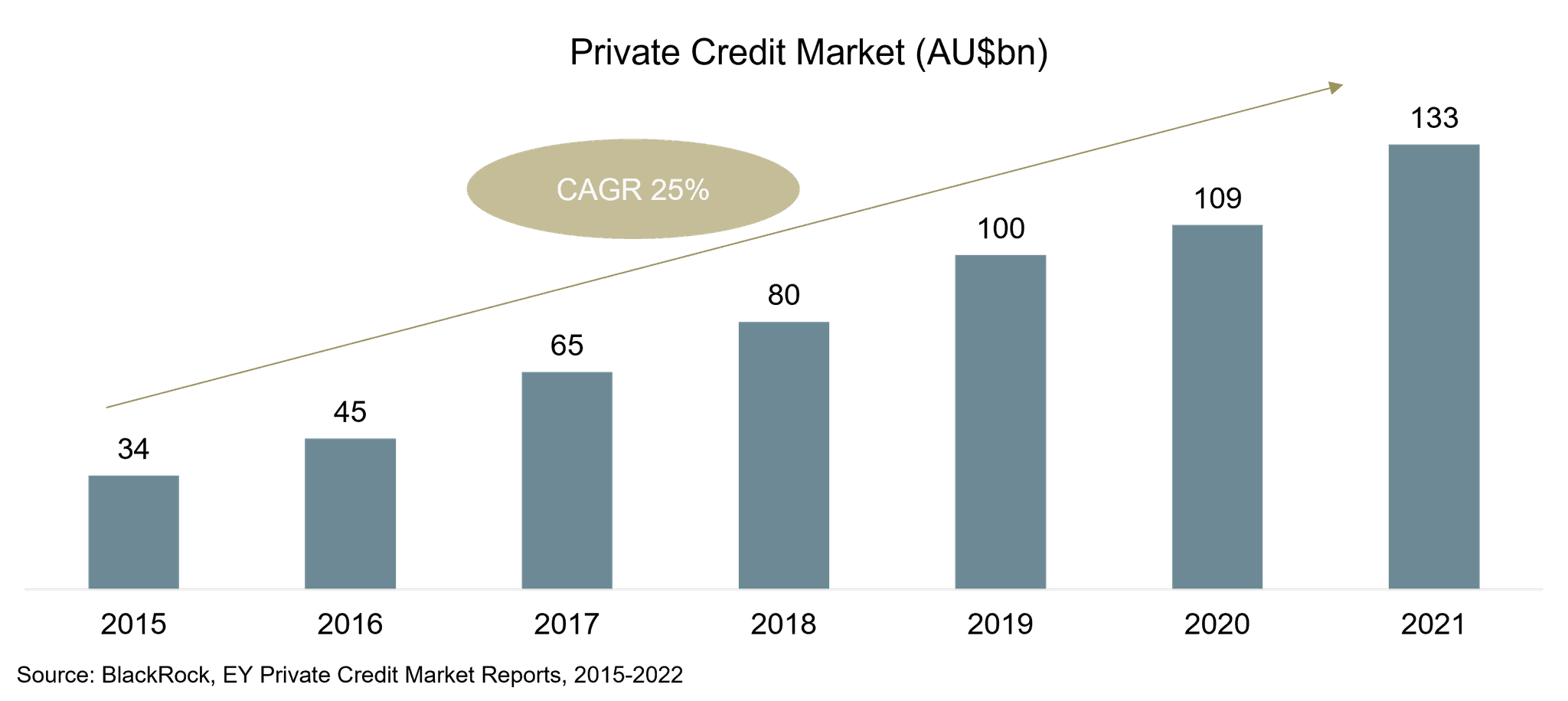

Traditional retail banks in the country are cautious when it comes to issuing new loans due to the regulatory environment, high capital requirements, and low-risk appetite. Based on the latest report published by EY and Australia Investment Council, non-banking lending contributes AU$1.2 billion to the Australian GDP and supports over 10,000 jobs in the country.

As gateways to Southeast Asia and Greater China, Singapore and Hong Kong have legal and bankruptcy systems similar to developed countries such as the US and UK. It is common for holding companies to be established in these cities while running operations in other developing cities due to their professional workforces, hi-tech setups, and/or tax benefits. Loaning to those companies could enable lenders to take advantage of a well-established legal system while tapping a wider variety of opportunities in the region. Furthermore, due to the increasing dry powder in PE/VC, private debt financing has been preferred over traditional bank loans for flexibility and negotiability.

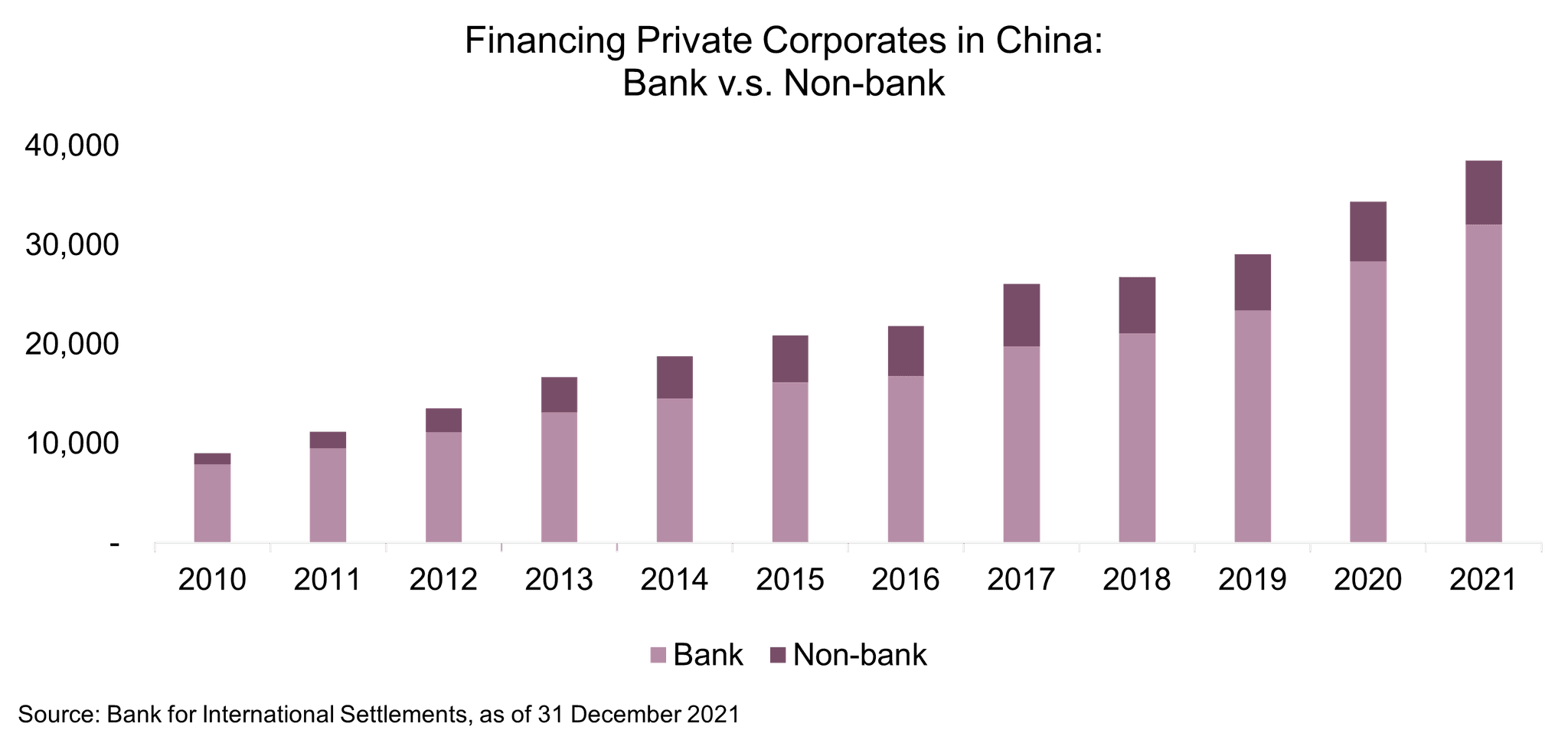

China

Recently, global investors have been contemplating whether China remains an attractive investment. Our local Petiole team remains confident in the nation's long-term growth potential as China continues to play a dominant role in the outlook for the emerging region.

After a series of lockdowns across the country and the Dynamic Zero-COVID policy during the first half of 2022, eased measures were announced in June, including a shorter quarantine period. Over the next few months, as China's travel restrictions are expected to further be relaxed, its GDP is predicted to grow again with China's relatively low inflation, a favorable monetary policy, and strong exports.

As part of Petiole's diversified private market investment programs, we have been harnessing private credit's potential over the past decade.

Contact our expert team today to find out more about how private credit/debt can be valuable to your investment requirements.