As part of Petiole’s real estate strategy, we eyed London’s West End, one of the world’s most prestigious districts.

Brexit, the COVID-19 pandemic, and supply chain worries hit London real estate prices hard over the past 18 months. Demand fell out of the commercial property market, sometimes with no bid whatsoever, as offices emptied, and most people were forced to work from home.

But while most areas of the city have seen falling rents, the West End property market has turned a corner. We partnered with one of the top European real estate sponsors to acquire a leasehold asset for refurbishment, lease-up and sale located in St. James's, just steps away from Trafalgar Square. Here’s why.

Pandemic-proof

Bidding in the West End real estate market has been competitive, and yields remained strong throughout the pandemic. The recent sale of a property on Waterloo Place for GBP 72 million (GBP 2,006 per sqf) in February 2020 is one of the best comparisons to ours – it was newly refurbished in a very similar location and is also held on a long leasehold. Due to COVID, we managed to acquire this property at a significant discount compared to others in the area.

Significant Undersupply

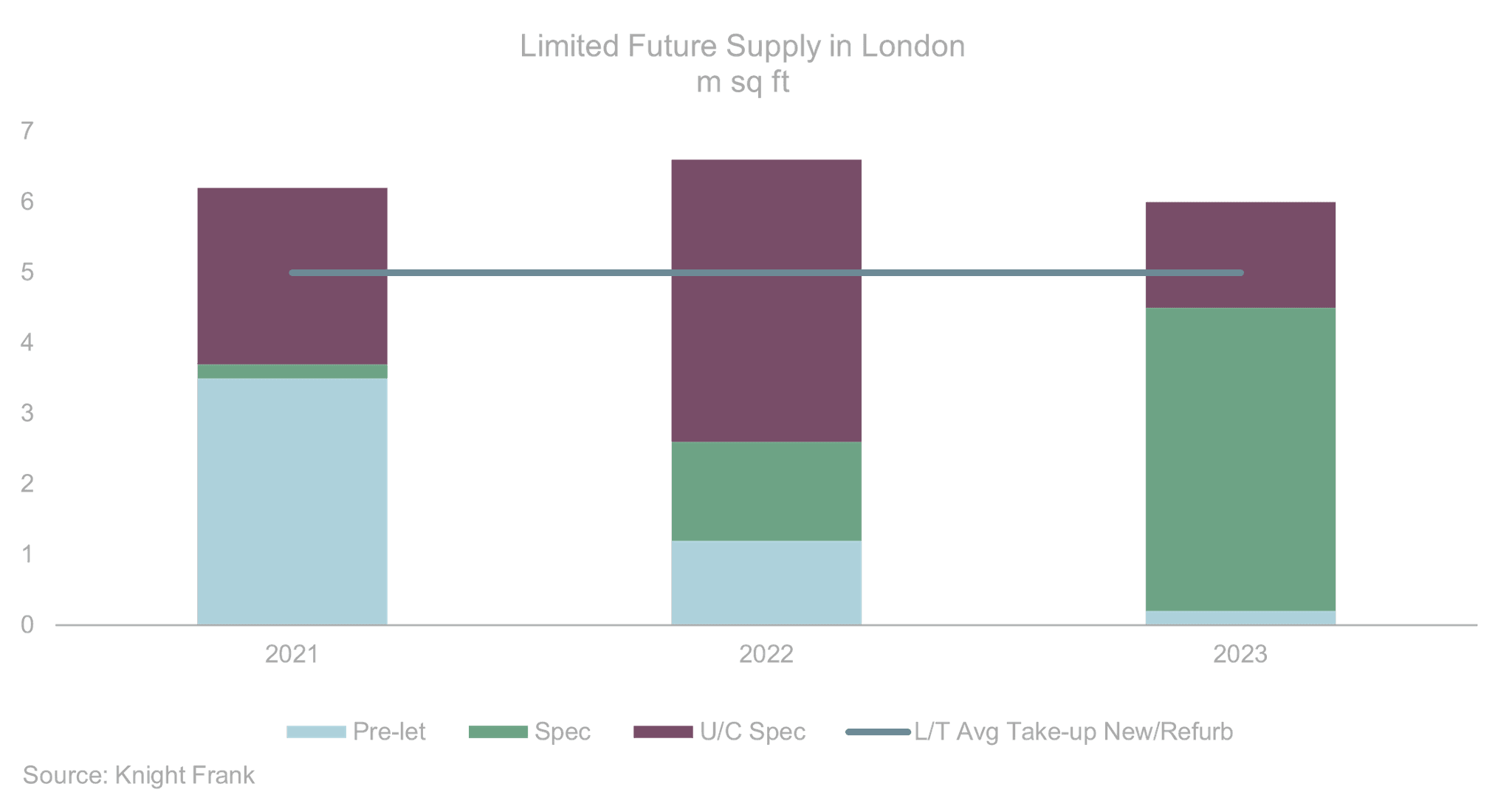

Knight Frank' analysis of the development pipeline data shows c.19.1m sq ft of completions in 2021-2023 and pre-lets comprise 27% of this total. Therefore, c.14m sq ft of space is speculative of which 6.4m sq ft are pipeline schemes that have not been started and may not complete during the next three years. This leaves c.7.5m sq ft of speculative space which is currently under construction and compares to a three-year average take-up of new and refurbished space of c.15m sq ft.

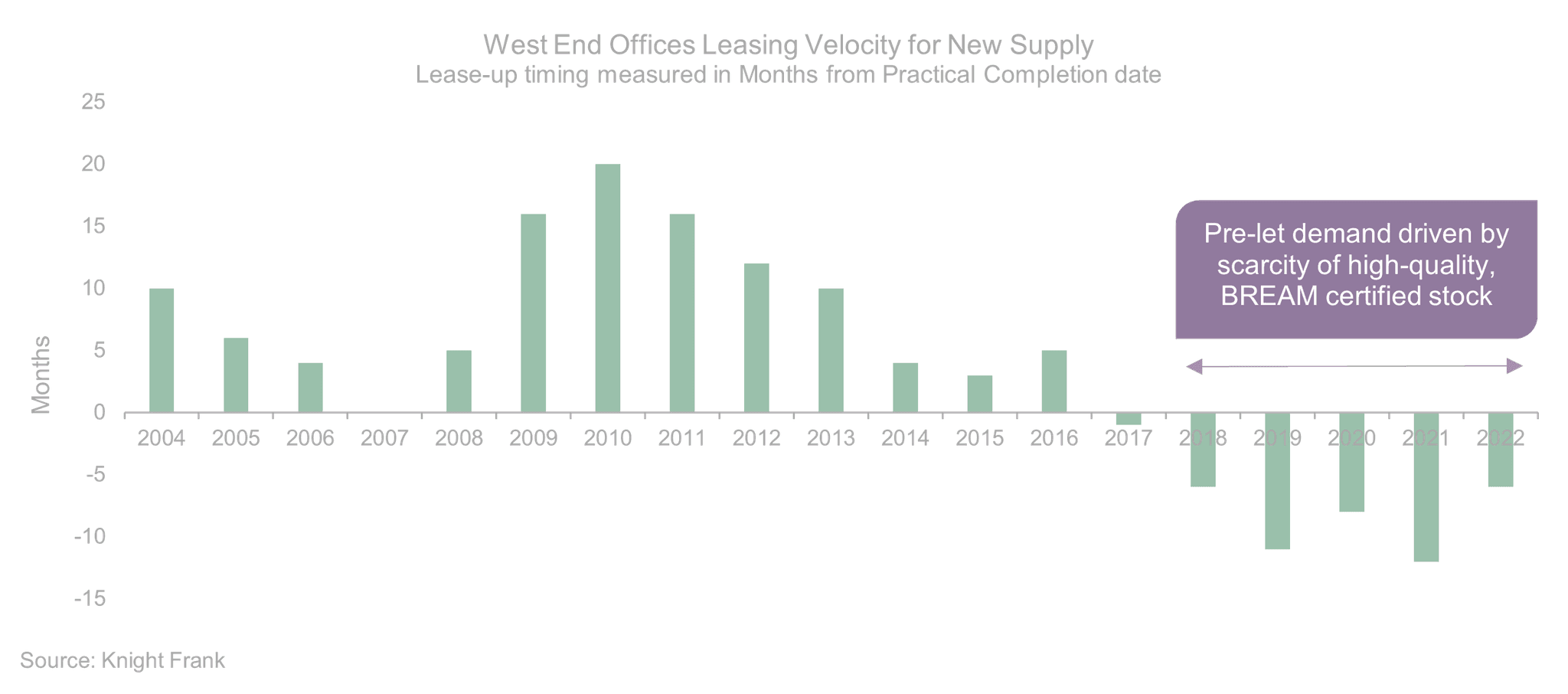

There is a particularly limited supply of ESG – Grade A properties in London even though regulators demand high standards and society expects it. In fact, for the past three years, a full lease-up time for ESG high-quality assets was averaging six months before completion of the refurbishment.

The impact of ESG demands on real estate players is heavy, with everything from taxes, regulatory requirements, strategy, and operations being affected. The pandemic has accelerated this positive change but also highlighted just how few properties can meet the high ESG bar set by the rest of the world.

International real estate consultant Knight Frank recently revised upward their 5-year rental growth forecast for West End Core properties from 11.8% to 15.1%. Additionally, St. James’s vacancy rate remains low at 3.3%, while the availability of newly refurbished stock is even tighter (c.1% vacancy), driven by demand from occupiers wanting to upgrade their offices.

Significant Crown Estate Investment

The Crown Estate, which is a collection of landholdings belonging to the British Monarchy, is investing a minimum of GBP 500 million into improving its St. James’s real estate portfolio up to 2025. The Crown owns about 50% of freehold interests in this area, as well as the entirety of Regent Street, and it is one of the largest property managers in the United Kingdom, with properties valued at GBP 9.1 billion. The St. James's program seeks to enhance the borough as an exceptional business address and preserve the unique architectural and historical character of the area. Consequently, this has encouraged neighbor landlords to invest in improving their own assets.

There is something about this part of the capital that exudes timeless prestige. The neon lights set against the alluring mix of the old and new. The vibrant energy, cosmopolitan flair, and the sense of having the world at your fingertips. Of course, these benefits shouldn’t blind us to the real slowdown caused by the pandemic, along with Brexit, which ushered in its own challenges. But together with all the other market forces, West End property has become attractive as an investment.

Ultimately, we believe that the freehold-leasehold arbitrage, limited supply of refurbished or ESG-compliant properties in the pipeline, large investments by the Crown, and the long-lasting prestige of the area are all positive underpinnings for our newly acquired West End asset. Moreover, real estate offers protection against inflation as inflation expectations are rising. This fits into our Capital Growth offering.