As private assets assumed a vital role in asset allocation over the past decades, the secondary market for these assets has grown rapidly and is becoming an essential portfolio management tool for asset allocators.

Overview

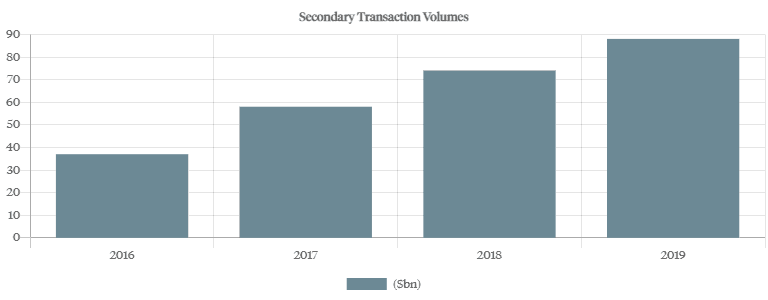

Since 2016, the secondary market has grown from $37 billion of transaction volumes to $88 billion in four years representing a 16% CAGR from 2016 to 2019. It has turned into a robust marketplace with sophisticated investment strategies, dedicated analyst coverage, and technological platforms. Many reasons lead investors to seek liquidity through the secondary market: an investment exceeding its original time horizon, a prolonged harvesting period where no upside could be earned, a changing investment mandate, or other reasons idiosyncratic to an investor. The channels in which investors take towards an exit include brokered auction processes, direct sales to secondary funds, or sales to counterparties with whom the investor has existing relationships. A secondary process could take several months and involves choosing a channel, testing the market, setting up data rooms for auctions, agreeing on a bid price, and finally transferring ownership.

The Secondaries Cycle

Secondary strategy returns arise from three main sources at different stages of an economic cycle. At the trough of a cycle, there is often a dislocation where forced selling creates an attractive margin of safety for buyers despite the true value of the underlying asset remaining uncertain. The dislocation is reflected as a percentage of Net Asset Value (NAV) and certain cyclical industries such as energy are susceptible to larger swings in price. As recovery gains traction, pricing begins to converge with NAV. Finally, at the maturity phase of the cycle, fundamentals’ growth begins to plateau, causing certain investors to resort to financial engineering and leverage to gain incremental returns.

Historical Trends

Previous market corrections have resulted in temporary periods of volatility followed by extended downturns, both of which have consistently benefited secondary investors. On the supply side, such periods brought more motivated sellers with potentially fewer reservations over price. On the demand side, careful selection is needed as the underwriting of secondary purchases is dependent on the asset-level fundamentals and strength in the aftermath of a downturn.

"Buyers focused on asset selection generally have better opportunities to acquire specific assets at attractive values during times of crisis."

In the years following the Global Financial Crisis of 2008 (GFC), intermittent volatility in public markets and a private market downturn drove increased selling into the secondary market. Secondary funds emerged providing opportunities for sellers to access liquidity, and for buyers to achieve superior risk-adjusted returns.

Secondaries after the COVID-19 Price Shock

At the onset of the COVID crisis, private equity sponsors continued to buy assets through add-ons and distressed investments, while most conventional exits were put on hold to avoid discounted pricing. From mid-March until July 2020, secondary market activity ceased almost entirely, primarily because market participants did not know how to price deals amidst unprecedented uncertainty. As a result, most portfolio sales were put on hold until Q3 2020, giving time for public markets to recover most of their losses and allowing Q2 2020 marks to reflect management guidance more accurately.

"The initial period of extreme volatility in the public markets appears to have ended, but the window of opportunity for PE secondaries could remain open for some time."

Most secondary opportunities have just recently surfaced, and volumes could continue to ramp up over time like they did after the GFC, creating attractive buying opportunities. Although this period of price discovery was much briefer than the one following the GFC, more secondary opportunities may still take time to emerge as investors gain more clarity and become more comfortable with an underlying asset’s positioning in a post-pandemic world. Additionally, there is $150 billion of dry powder under the secondary asset class which could potentially minimize the gap between price and NAV.

Petiole and PE Secondaries Market

Petiole has frequently engaged in markets for secondaries, both as a buyer seeking attractive investments and as a seller for seeking exit opportunities. Of particular interest for our secondary market allocation is Asia, where we co-invested alongside niche sponsors in secondary deals transactions where market and pricing inefficiencies still exist.