Can real estate hedge well against inflation? Read how this asset class has historically performed during such periods and which sub-sectors fared better than the others.

Real Estate Against Rising Inflation

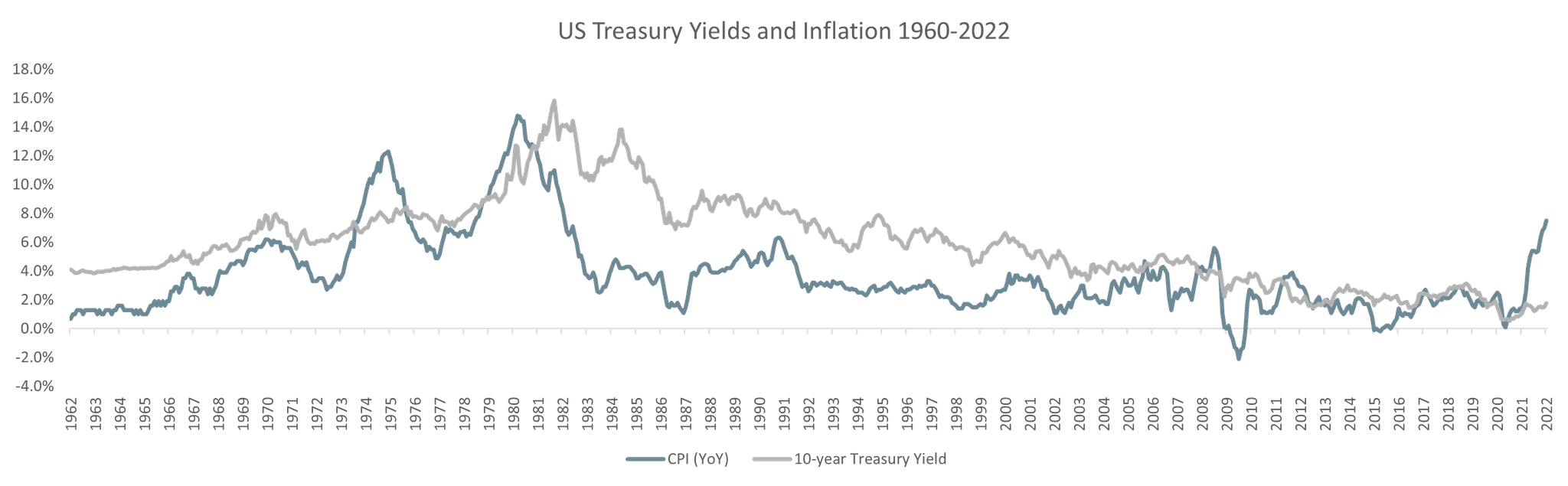

Inflation has surged around the globe over the past year. In the US, consumer prices rose at an annual rate of 7% in January, the fastest pace in 40 years. (1) Meanwhile, eurozone inflation broke records for the third month in a row, rising to an annual pace of 5.1%. (2)

Having spent much of last year telling markets that inflation would prove temporary, some major central banks have started to accept they are facing a more persistent enemy. Federal Reserve chief Jerome Powell, for example, recently said that the central bank was likely to increase rates in March and end the extraordinary monetary support it has provided to the economy during the pandemic. (3)Who Let the Inflation Genie Out of the Bottle?

Two factors have combined to ignite this burst of inflation. Authorities around the world responded to the outbreak of the COVID-19 pandemic by imposing lockdowns that had a catastrophic impact on economic output as factories closed their doors. At the same time, huge injections of government aid and ultra-low borrowing costs helped spur demand for goods, particularly as economies emerged from pandemic-related controls. But supply chains remain squeezed by shortages of labor and raw materials, and the imbalance between supply and demand has inevitably resulted in rocketing prices.

Financial Markets Take Fright

Having enjoyed strong returns in 2021, global stock markets fell sharply in January as the prospect of higher interest rates took hold. The MSCI World Index fell by nearly 5% in dollar terms, while bond yields spiked. The yield on ten-year US Treasuries ended January at 1.78%, up from 1.51% at the end of last year, while the yield on Germany’s 10-year benchmark government bond rose above zero for the first time in three years, and corporate-bond spreads widened.

Inflation: The Main Enemy of Bonds

Over the longer term, inflation is likely to pose less of a threat to equities than to fixed income. That’s because company earnings—particularly the earnings of companies with strong pricing power—generally rise along with inflation.

By contrast, during the high inflation of the 1970s, bond yields soared and bond investors suffered significant losses as prices moved against them.

Not All Sectors Are Equal

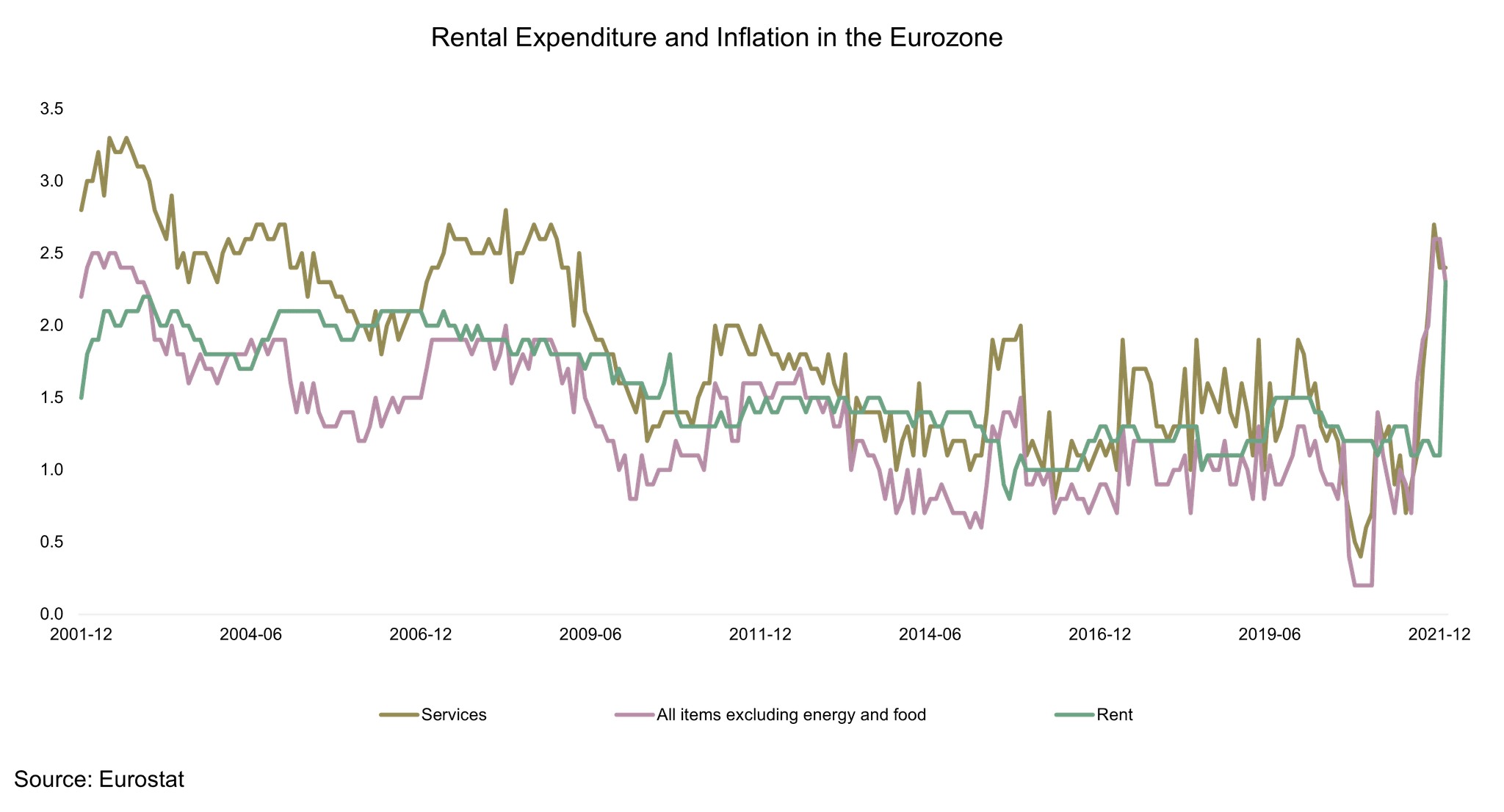

As with any asset class, it pays to take a selective approach to investing in real estate. Multifamily, for example, can prove a good hedge against inflation. That’s because the leases on individual rental units tend to be renewed annually (unlike some commercial properties, such as retail outlets, which usually have multi-year business leases), providing a more frequent opportunity to adjust the rent in line with inflation.

Be cautious, too, of trends driving individual sectors. While rising economic activity should drive demand for real estate, the pandemic has had a dramatic impact on behavior, which could prove permanent. The prospects for office-space rental income, for example, are now less certain, given that the shift to hybrid working could affect long-term demand.

In addition, as more people work from home, they are staying away from urban centers and retail parks. A recent report by Retail Economics and the e-commerce tech firm Metapack estimates that US$650 billion of global non-food spending will permanently shift online by 2025. It adds that 20% of consumers say they will continue to shop more online, long after the impact of the pandemic has subsided. (4)

Conversely, demand for warehouses that are central to e-commerce is exploding. Micro-fulfillment centers (or relatively small warehouses in urban locations) are proving particularly popular, while their supply is limited. That reflects the trend of consumers becoming increasingly demanding and expecting almost instantaneous deliveries.

The multifamily space has also benefited from pandemic-related themes. The rapid rise in home values triggered increased demand for multifamily units. Remote work and pent-up demand for open space post-quarantine led to a flight from cities and increased consumer demand for suburban housing in markets that were previously underappreciated. At the same time, median home price appreciation accelerated in late 2020, with Zillow reporting a year-on-year increase of 10.6% as of March 2021, the largest increase since March 2006 and well above the 10-year rolling average of 4.2%. Consequently, more aspiring buyers found they were unable to afford a home and opted for suburban rentals instead. This has presented opportunities to invest in a resilient market with limited supply.

Conclusion: Real Estate Can Prove as a Useful Shelter Against Inflation but Depends on Where You Invest

Higher rates of inflation than many investors have seen in their lifetimes are likely to persist in 2022 and possibly next year. There is also a danger that once entrenched, inflation may not subside for some time.

It is also important to note that the long-term, relatively illiquid nature of real-estate assets underlines the need for exposure to sectors where long-term secular growth drivers can be identified.

Key Takeaways

Rental income is the key driver of returns in the real-estate sector, and rents have traditionally moved in line with or above inflation.

The current outlook of rising economic growth and demand-driven inflation augurs well for the real-estate sector.

Investors need to be aware of the long-term drivers of demand in particular sectors of the real estate market.

With 18 years of track record in private real estate investing, you can contact our team to learn more about Petiole's investment solutions in this asset class.

References

Inflation at 40-year high pressures consumers, Fed and Biden, Associated Press, 12/01/22

Eurozone inflation hits new record for the third month running, Al Jazeera, 02/02/2022

US Federal Reserve says rate rise ‘appropriate’ soon, BBC News Online, 26/01/22

E-commerce Delivery Benchmark Report 2022, Metapack and Retail Economics