COVID-19 has affected us all in different ways, and the financial markets are no exception. While we have seen negative effects such as slower transaction activity and lower levels of fundraising, private equity vintage performance should rise – a common occurrence following periods of widescale economic disruption.

The Effects of COVID-19 on the Private Equity Market

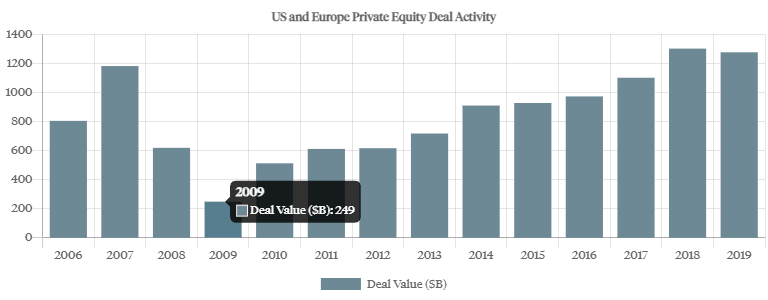

Deal activity slowed significantly in 2020 following two full quarters of COVID-19 impact. As of September 30, activity volume year-to-date in the US in terms of dollars was down 37% compared to the same period in 2019. In terms of transactions closed, activity was down 33%.

By the end of the third quarter in 2020, global fundraising for the year was $400 billion, compared to $480 billion for the same period the year before, according to Pitchbook’s and Preqin’s Q3 2020 reports.

The percentage of add-on deals increased to 58% of all closed deals. This confirms that sponsors were continuing to focus on these types of transactions as opposed to leveraged buyouts.

Over the past decade, increased competition, availability of cheap financing in a low interest rate environment and increasing pressure from investors to deploy rising dry powder (committed but unallocated capital) all contributed to a significant expansion of the average valuation multiples, from 7.5x in 2009 to highs of 15.2x in Q2 2020. However, in the third quarter, the rolling four-quarter median multiple dropped to 12.9x as average debt fell from 6.9x to below 6.0x.

"Consequently, COVID-19 has given further cause for scrutiny over adjusted figures as many companies are reporting EBITDA figures with specific pandemic-related adjustments."

Moody’s issued a report warning that these coronavirus adjustments are highly hypothetical and subjective. We advise that proper selection is paramount in this environment.

Secondaries Market Activity Has Also Slowed

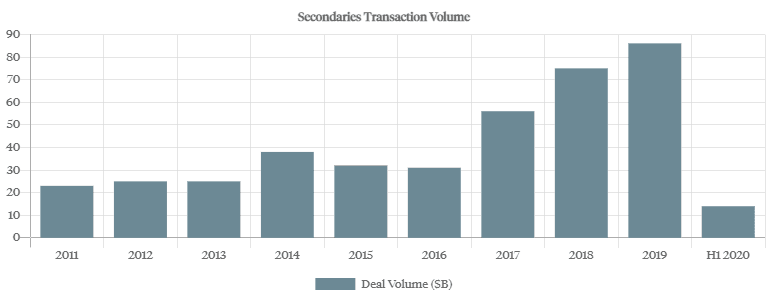

Following the COVID-19 outbreak, the secondaries market ceased almost entirely from mid-March until July. This led to a 65% YOY (year-over-year) reduction in transaction volume to $14 billion in the first half of 2020, from $40 billion in the first half of 2019. Volumes have staged a partial recovery since August, however, according to managers in this space.

The decline in deal activity has increased industry dry powder from $110 billion in 2019 to $120 billion in the first half of 2020. This large and rapidly growing amount of dry powder will help to keep prices elevated over the medium to long term despite market volatility, except for heavily distressed assets.

The secondaries market has historically been segmented into two types of transactions:

Traditional, in which LPs transact

GP-led, in which GP interests are transferred towards the tail-end of the fund, usually when the fund is reaching its term

GP-led transactions are now becoming the more common of the two transaction types and are expected to be the main source of sellers in the next 12 to 24 months.

Private Equity During Difficult Times

It is commonly understood that private equity outperforms public equity over the long-term. The assumption is often made that these return premia are a result of increased risk taking which is undesirable in times of crisis.

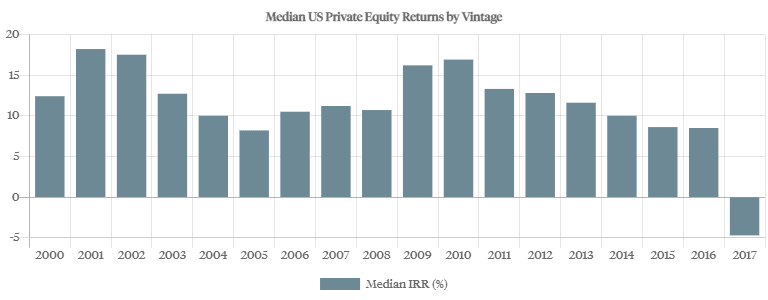

"However, as the median vintage returns from US and European private equity sponsors show, private equity actually has the best vintages following turbulent macroeconomic periods, such as the world is currently experiencing."

Notably, private equity sponsors tend to deploy in sectors that are more insulated from the crisis. For example, popular themes observed among private equity managers during COVID-19 have been:

Education services

At-home fitness

Pharmaceutical services

Healthcare IT

- Digitally native brands.Source: Cambridge Associates

This return outperformance in private equity versus public equity is furthermore attributable to a few key factors:

More thorough company-operating information derived in the due diligence phase, inaccessible to a public-markets investor

Active corporate engagement with a company’s management to implement operational and strategic improvements

A longer-term value creation plan beyond the quarterly or annual horizon that public companies operate at

When combining these factors with the strong selection process and lower entry valuations, it becomes clear why the best time to invest in private equity is in fact during difficult times.