Recent years have shown an increasing interest among private equity firms in carving out non-core business units from their parent companies - a strategy that presents a unique opportunity to achieve superior risk-adjusted returns. The current pandemic may catalyze a heightened adoption of this strategy over the next years.

Overview

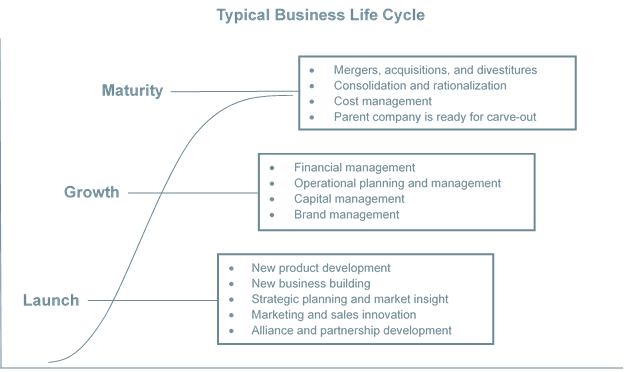

A corporate carve-out occurs when a parent company divests a business unit. The parent company typically disposes of a non-core business to create value by using the proceeds to a) invest in core capabilities that enhance its competitive edge, b) reduce debt, or c) improve earnings per share by reducing capital through dividends and share buy-backs.

In theory, corporate carve-outs are simple: a private equity firm invests in an undervalued, mismanaged asset that has growth potential, implements value-creation strategies to promote growth, and exits at a higher valuation. However, considerable risks and level of complexity are associated with its execution.

"It is of paramount importance for a private equity investor to be certain that value can be created from a carve-out once it is separated from its parent organization."

For a private equity investor, a carve-out often represents an attractive opportunity to improve the stand-alone value of a non-core asset by focusing the business strategy on optimizing operations, or identifying needed financing to exit the investment profitably through its sale to a strategic investor, an IPO, etc. A private equity investor in carve-outs may undo negative synergies from its previous consolidation with the parent company.

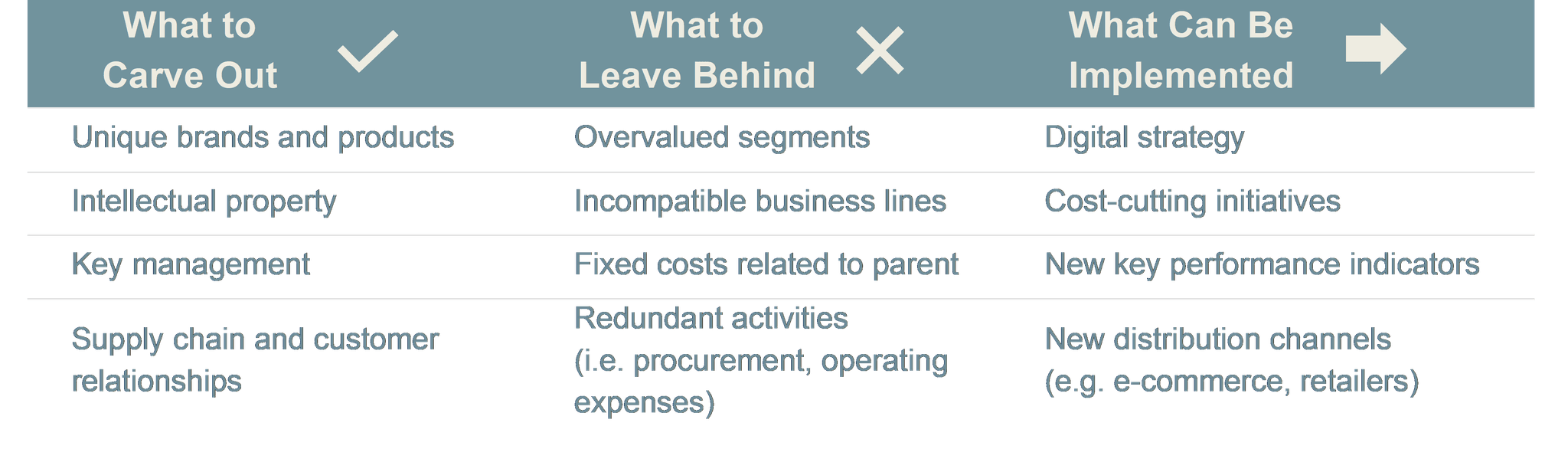

"The key is to identify carve-outs where value can be added without the parent company, and to shed any assets that are incompatible with the value addition."

In the aftermath of the COVID-19 pandemic, more companies might be compelled to sell non-core subsidiaries for their liquidity needs, which could present interesting opportunities for carve-outs in the near future. Amidst high economic uncertainty and potential for slowdowns, carve-out execution has become more and more complex, especially in cross-border settings where the pandemic has made on-site due diligence difficult to implement.

"The success of carve-out investment opportunities would greatly depend on the choice of partners with proven track record, experience and talent pool to execute the activity adeptly."

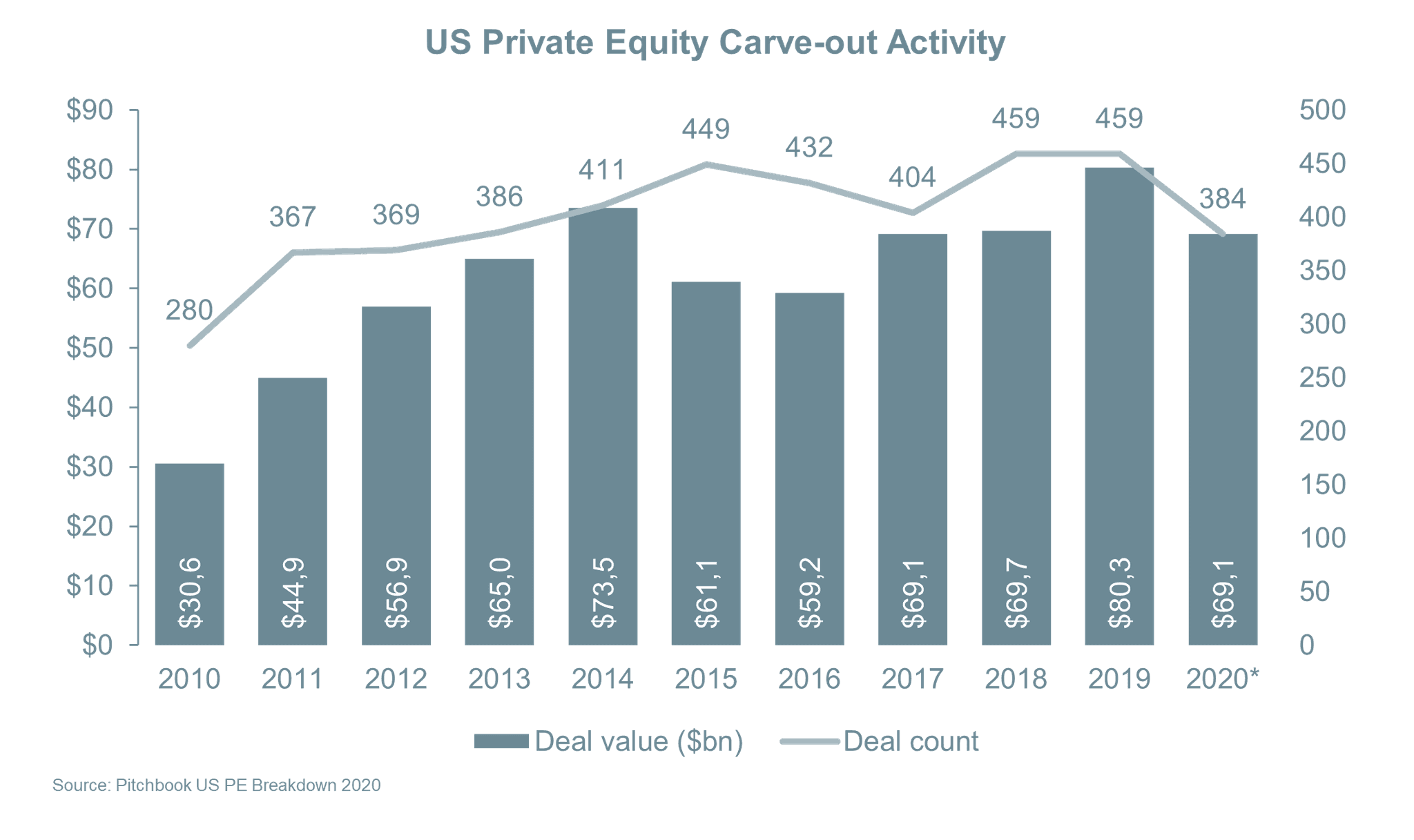

In Europe, record dry powder held by private equity funds is forecasted to boost carve-out activity in 2021, after a slump in 2020 which resulted in the lowest carve-out activity in the continent since 2013. Moreover, the excess liquidity provided by government stimulus is not expected to sustain companies throughout 2021, which may force some to ease liquidity through divestitures. The persistent anti-trust pressure from European regulators could also lead to an increase in carve-out activity. Across the Atlantic, the US faces a similar backdrop albeit with higher debt burdens, which can put more pressure on companies to sell non-core assets.

Corporate Carve-outs through Petiole

In the last three years, Petiole has invested in partnership with KKR in many corporate carve-outs, including Upfield, Hitachi Koki, Calsonic (now Marelli) and Hensoldt. In the most recent partnership with KKR in November 2020, Petiole invested in the acquisition of Wella from Coty Inc. Wella, a company headquartered in Darmstadt, Germany, is the second largest global professional hair player behind L’Oréal and has been part of Coty Inc. (NYSE:COTY) since its purchase from Procter & Gamble in 2015.

Strategic buyers could realize clear synergies in acquiring these companies after executing the value-adding activities. The opportune timing offers a unique way to invest in carve-outs before markets fully recover from the negative consequences of the pandemic.