The long-term outperformance of private markets over public markets has been encouraging investors to increase their allocation to this asset class. Constructing a portfolio that is unique to their investment goals is key, but which factors play crucial roles?

Despite the potential benefits of private market investments, there remains a risk of underperforming expectations. To achieve the enhanced potential benefit of private markets, investors must adopt best practices when it comes to portfolio construction.

As world-renowned investor Peter Lynch’s famously said, “Know what you own, and know why you own it”, building private market portfolios is a dynamic process, and with more than 18 years of experience, Petiole has developed a 5-factor approach to portfolio construction.

1. Long-term View

With private markets, staying invested over multiple years will matter. Therefore, the macroeconomic environment and trends shaping the world need to be considered because different geographies and asset classes within private markets react differently. An investor’s long-term views will influence the geographical and industrial exposure, as well as investment strategies. For example, as economies become more and more digital, cybersecurity will grow in importance, and exposure to cybersecurity- / data protection-linked assets could present pockets of opportunities.

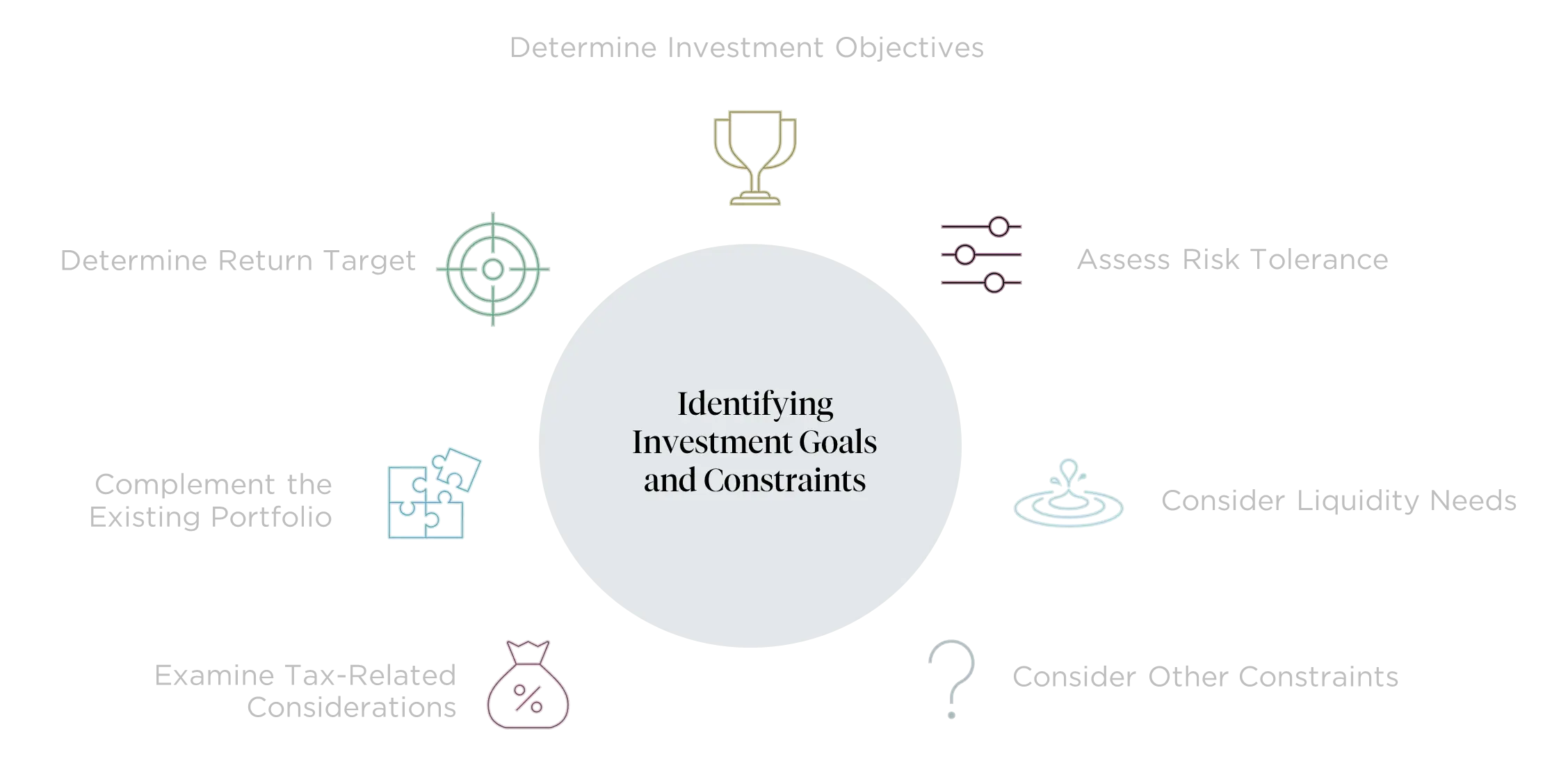

2. Goals & Constraints

Investment Objective: What is the Investment Objective (i.e Wealth Preservation, Income Generation or Wealth Appreciation)?

Return Targets: What is the risk an investor is willing to take to achieve potentially higher returns?

Liquidity Needs: What is the investor’s acceptable capital lock-up period? For example, will the investor need money over the 5-7 years to fund the purchase of a residential property or his children’s education?

Tax Issues: Do income distribution and capital appreciation have different tax implications in the investor’s jurisdiction? Income distributions in the U.S., for example, are taxed differently from capital gains, which may affect the motivation of U.S.-based investors towards income-generating assets.

Other Investment Constraints: Does the investor have other considerations (e.g. ESG) that limit the investment universe?

Complementing the Existing Portfolio: How can the private market portfolio complement the existing traditional investments?

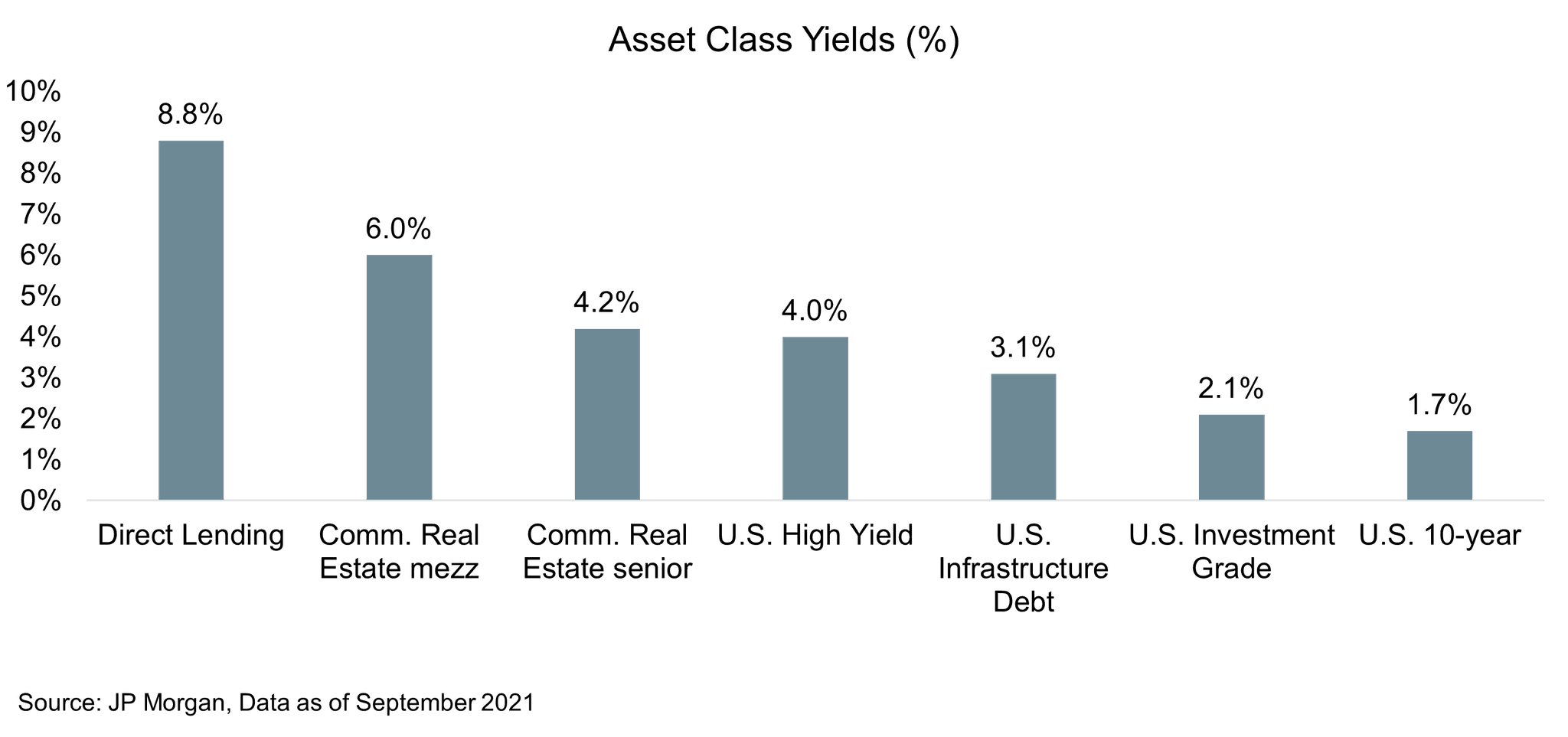

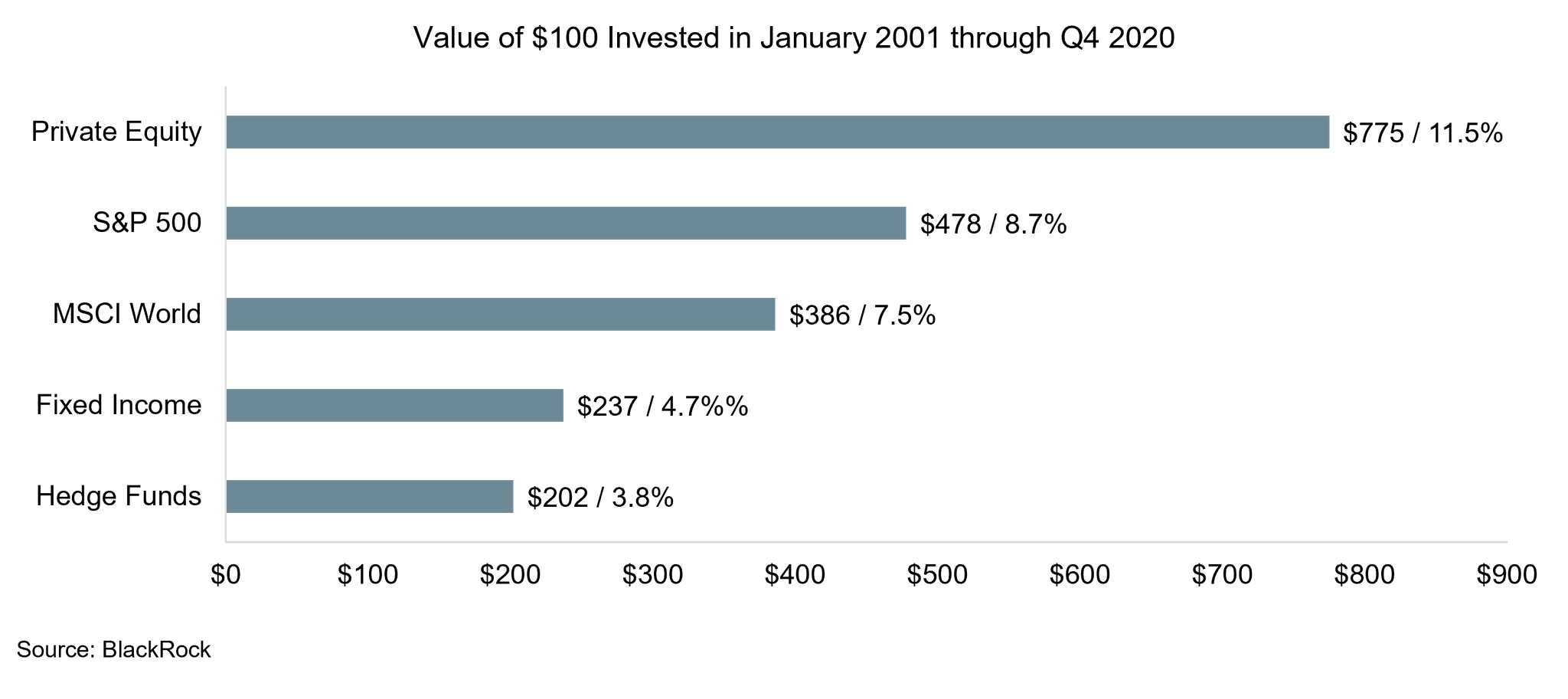

3. Asset Class Selection

Aligning the portfolio’s asset allocation with the determined objectives and constraints could be done by categorizing private markets into two main asset classes:

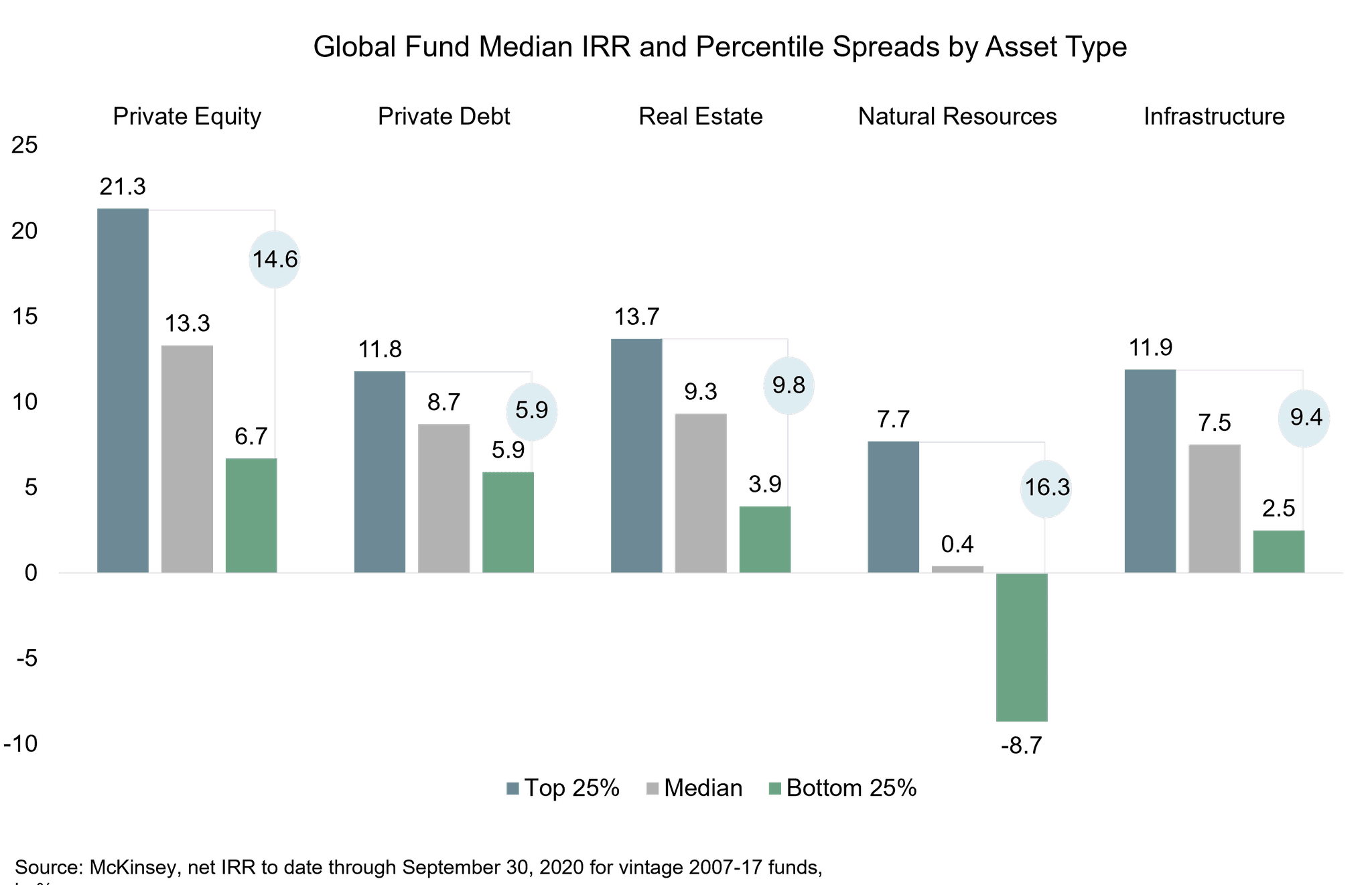

The next essential step is selecting the right sponsors and deals that fit well with the previously identified goals, constraints, and asset allocation.

A research by McKinsey reflects this analysis:

At the end of the day, private equity’s enhanced returns, relative to public markets, are a function of active management and value creation. The sponsor’s ability to buy businesses at an attractive value, provide growth capital, and participate in value creation (i.e. Growth Strategies, Margin Improvements, Management Incentive Schemes) - all these contribute to what distinguishes top quartile sponsors and managers from the rest.

While careful manager selection is of great importance, diversification by sub-asset classes, vintage years, geographies, and industries can also strongly help in reducing undue risk.

5. Ongoing Monitoring and Oversight

Constructing a diversified portfolio is just the start of a long-term and dynamic approach to investing in private markets. It is equally significant to keep track of performance and maintain access to the top GPs and opportunities in private markets.

Some of the aspects to consider include:

Cash Management: This includes managing capital calls and distributions, and using pacing studies to optimize liquidity needs to ensure there is enough cash on hand to meet capital calls.

Valuation: Obtaining and reviewing the quarterly valuations of investments would help to understand what is driving performance in the portfolio.

Monitoring: This involves a close watch on the underlying asset performance and valuation, comparing actual vs target MOIC, IRR, DPI, etc., and generally evaluating the sponsor performance.

A disciplined and dynamic approach to working with the right financial experts is a critical factor for success when structuring and maintaining a private markets portfolio.

Contact our private market experts who are ready to provide an unbiased assessment of your investment needs for a bespoke portfolio solution.

References

Historical Outperformance of Private Equity, Blackrock, July 2021

Prive Credit Investing Outlook, JP Morgan, 12/01/2022

Private Markets Come of Age, McKinsey&Company, February 2019