Multiple economic indicators point to challenging times ahead for investors. Here’s a summary of our market analysis providing insights into our investment approach in navigating through periods of uncertainties.

1H 2022 – A Look Back at Key Events

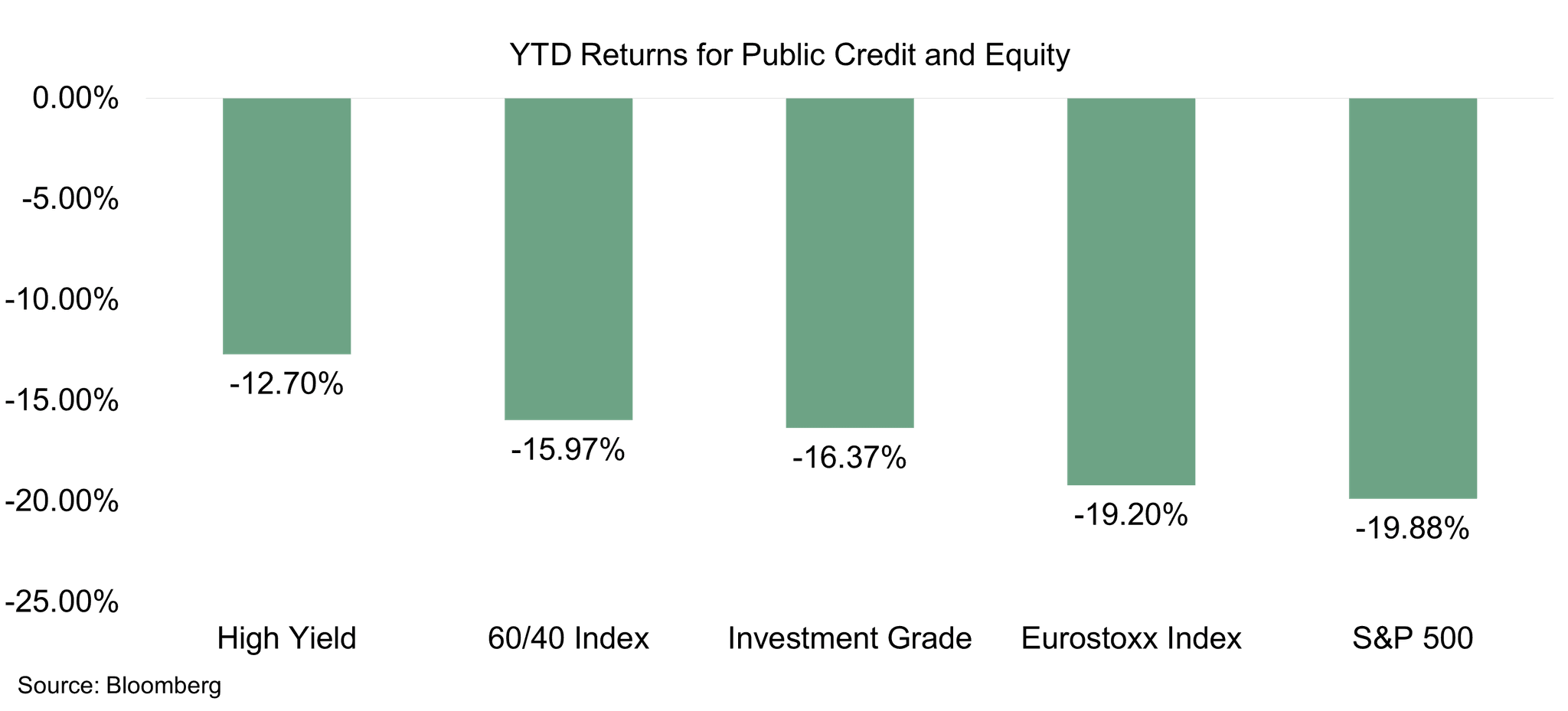

The first half of the year witnessed an accelerated deterioration in global economic conditions mainly due to the 4Rs: Russia, Rates, Risk and Recession. The Ukrainian-Russian conflict threatened international stability and triggered supply chain issues, trade frictions, and increased commodity prices. The stock market is off to its worst start since the 1970s, wiping out $3 trillion in retirement savings. Historic inflation readings, which reached an 8.6% year-over-year increase in May and 9.1% year-over-year increase in June, caused hawkish interventions from central banks, such as a 75bps rate hike initiated by the Federal Reserve - a move last seen in 1994 - with a potential 100 bps increase in July. ECB President Christine Lagarde recently warned that she “doesn’t think we are going back to that environment of low inflation”, while Fed Chair Jerome Powell said that restoring price stability was “likely to involve some pain” where the worst would come from failing to tackle the high inflation.

A combination of geopolitical uncertainty and unorderly economic figures is the perfect recession recipe as they largely depend on factors outside the Fed’s control. Despite strong numbers coming from the labor and housing markets, investors' sentiment remains skeptical while the Fed tries to navigate through worsening conditions to achieve a “soft landing”.

Are we already in a recession? As of July 1, the Atlanta Fed’s GDPNow tracker, a running estimate of real GDP growth based on available economic data, is pointing to a 2.1% decline in output in the second quarter, following a 1.6% decline in the first quarter. After high CPI reports, expectations of a slowdown in U.S. growth for the last two quarters were reflected in the inverting 2Y-10Y yield curve as it reached its deepest level since 2000, which historically has been a good predictor of a recession. Other indicators also cause concern, notably copper prices that exhibited a 30% decline from their most recent highs in 2022; a bear market in copper historically preceded every recession in the past 30 years.

Outlook for the Second Half of 2022

As investors brace for tightened financial conditions, geopolitical tensions are still vastly present with repercussions widely felt across the global supply chain, but more pronounced in Europe.

We expect the second half of the year to remain fragile in terms of macro indicators, with several red flags such as low ISM Manufacturing Index readings, deepening yield curve inversion, and tightening financial conditions. We believe that the main theme going forward is the FED’s position and capacity to subdue inflation while avoiding a hard landing, and the level at which earnings will reflect the new inflationary environment.

Furthermore, geopolitical tensions remain elevated as a Russian embargo could significantly affect natural gas flows to Europe with “catastrophic” consequences for the global market, especially on GDP in the Euro area as the EUR continued its decline, reaching parity with the USD for the first time in 20 years.

At the start of the year, we advised investors that we're heading to a new phase: from low inflation to high inflation, low interest to high interest, and less volatility to more volatility. Therefore, we kept a large amount of dry powder.

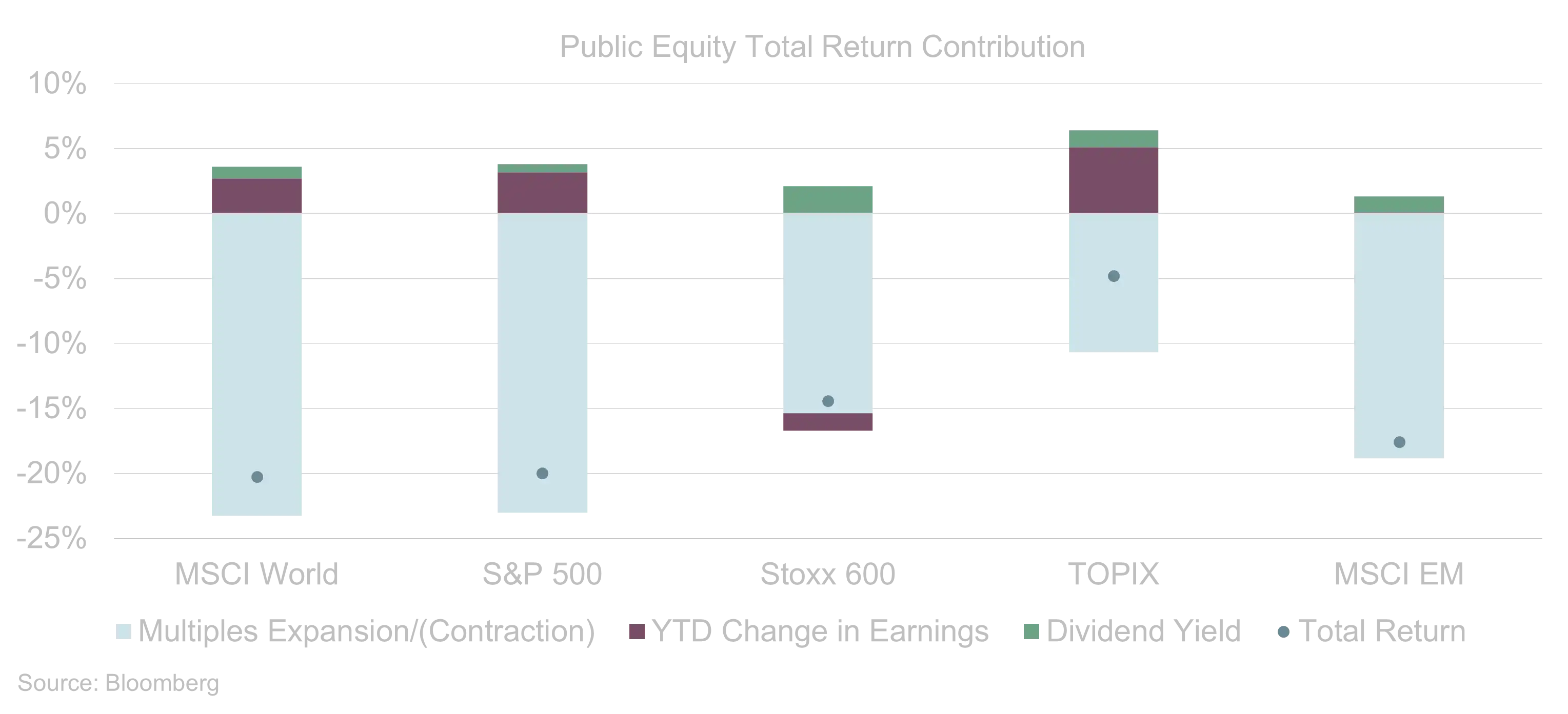

Where do we stand now? We see inflation continuing to be sticky in the short term, interest rates continuing to go up, and volatility remaining high. However, the big change to the start of the year has been valuations, as the sell-off we saw in the first half of the year moderated valuations across asset classes and removed the excesses in the market.

Our team diligently spent time assessing the macro picture, conferring with many sponsors globally, and outlining the current and expected market opportunities for the next 12 months. Two themes relating to the credit asset class emerge as our current focus:

High yield, loans, structured credit - where we are seeing dislocation and technical sell-off mainly from mutual funds

The financial sector - namely, U.S. community banks where valuations are attractive, balance sheets are healthy, and are inflation beneficiaries

The areas that we are focused on today are more public in nature and expressed in our dislocation themes. While we are private market investors, we do not shy away from expressing our views in the public markets in times like these when public markets offer us the ability to make sizeable returns without the need to be illiquid. Having been invested in private markets for many years, we recognize that it will not take long before the market re-prices for the private market asset classes which we started to see happening in our deal pipeline, particularly in the private debt and real estate debt space.

This environment strongly reminds us of the importance of staying committed to a rigorous investment process and a disciplined approach to investing. Through nearly two decades of investing across varying economic conditions, we have appreciated the value of long-term focus, thoughtful deal selection, prudent risk management, and portfolio construction.

Contact the Petiole team today to know more about our expert views on the current and future investment landscape.