Despite tracing its roots back to the 1970s, structured credit has yet to find a permanent allocation in traditional portfolio construction. With investment grade and high yields spreads at pre-crisis levels, and interest rate sensitivity considerations becoming paramount, structured credit stands as an attractive alternative.

The Structured Credit Universe

Since the inception of structured credit in the U.S. in the 1970s, this asset class has gained traction as a relevant alternative component in fixed income portfolios. However, despite its longevity and ability to generate alpha, it is still perceived as esoteric and inherently more risky than conventional fixed income. Some of this stem from the Great Financial Crisis of 2008, when the securitization of subprime mortgages in mortgage-backed securities (MBS) and collateralized debt obligations (CDOs) led to the financial meltdown. Other key reasons, though, include the scale and complexity of the asset class.

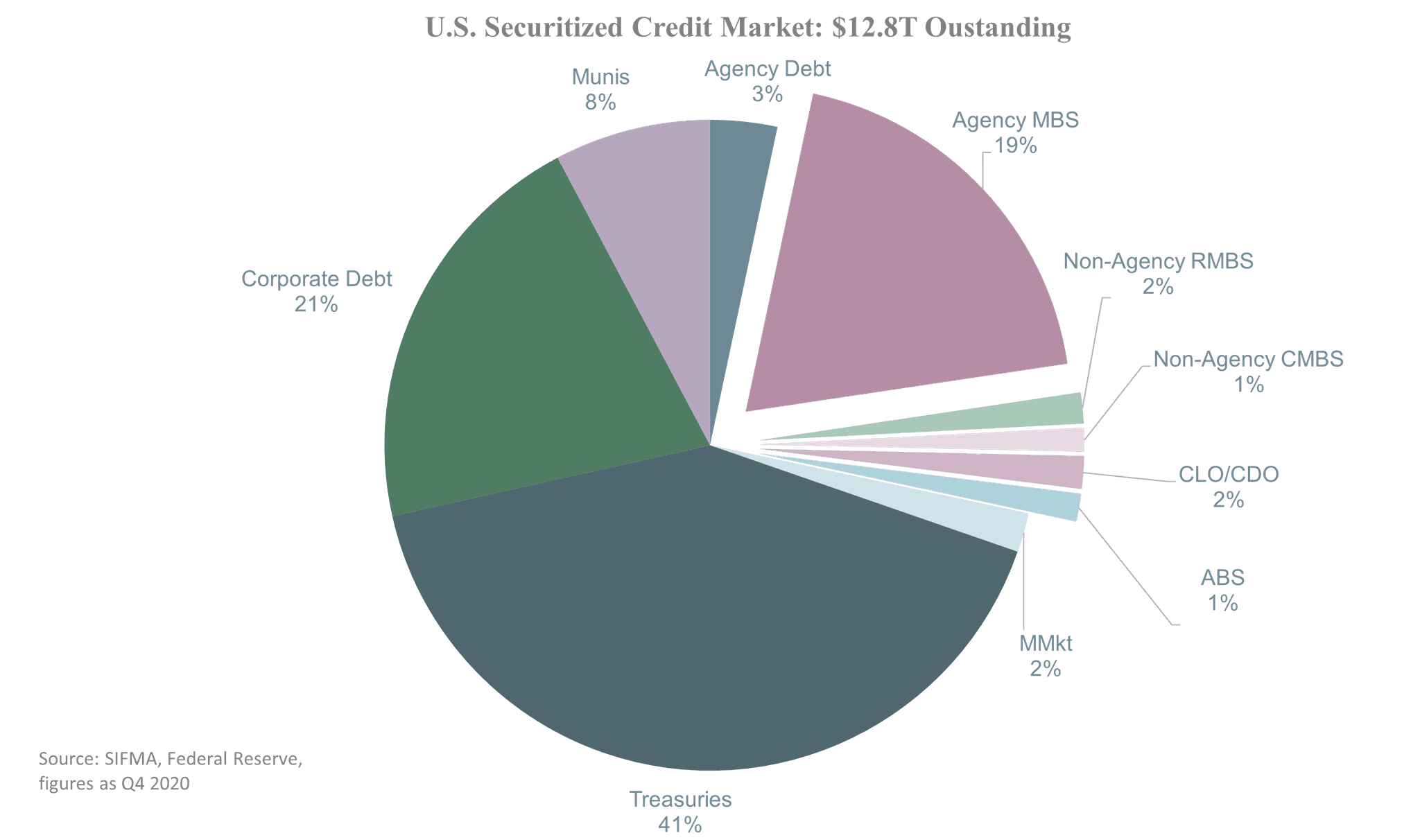

The U.S. securitization market comprises around 25% of the total U.S. fixed income market and consists of a diverse subset of securitization types. The largest relates to commercial and residential MBS securities, either agency or non-agency, representing $11.2 trillion. The market also encompasses collateralized loan obligations (CLOs), i.e securitized pools backed by 1st lien corporate loans, and asset backed securities (ABS), i.e securities collateralized by loans or leases on a variety of alternative consumer, commercial, or whole business assets. Common examples among consumer assets are auto loans and students loans, while common among commercial are shipping containers and aircraft. The asset class thereby offers a large, diversified investment opportunity across the full scope of the economy.

Market Opportunity in Today’s Environment

In today’s yield-starved market environment, alternative asset classes are becoming more prevalent in portfolio construction.

"Structured credit stands out as an attractive and viable alternative given the qualities and opportunities it presents."

Higher/tailored yields:

· Higher yields available today versus other debt instruments of comparable risk

· A complexity premium which embeds higher spreads compared to conventional assets, despite the inherent diversification they possess

· A number of sectors and securities trading below their intrinsic value

· Ability to tailor the return profile by investing across tranches

Structural enhancement:

· Floating rate products, systematically hedging against inflation and interest rate risks

· Credit enhancement through subordination (the tranching of losses) and over-collateralization (the balance of underlying assets exceeding the balance of the tranches)

· Risk retention by seeking to align the manager with the investors, whereby the manager retains an economic interest in the underlying assets (Although not mandated in the U.S. anymore, many managers seek to comply with this to meet requirements in the Eurozone and Japan)

· Increased disclosure and reporting, requiring both issuers of structured credit securities and rating agencies to disclose to investors asset-level information and enforcement mechanisms

Diversification:

· A pool of assets that would need to see industry-broad defaults for the structure to fail (for example, a typical CLO consists of around 150+ bank loans)

· The ability to take advantage of both the new issuance in the primary market and relative value trades in the secondary market

· A historical lower correlation versus other fixed income categories

Attractive New Issue Spreads

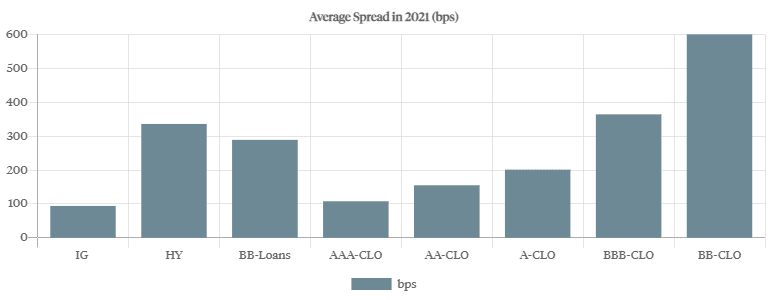

The higher yields in structured products today are well observed in the recent new issuance market. The following graph shows the 2021 average spreads in the U.S. of new issue CLOs versus investment grade bonds, high yield bonds and senior secured loans. For example, the average of the investment grade tranches of new issue CLOs is 207 bps, versus the 94 bps of investment grade bonds. Likewise, BB CLOs have an average spread of 600 bps versus the 336 of high yield bonds and 289 bps of BB senior secured loans.

New Issuance Volumes Rebounding

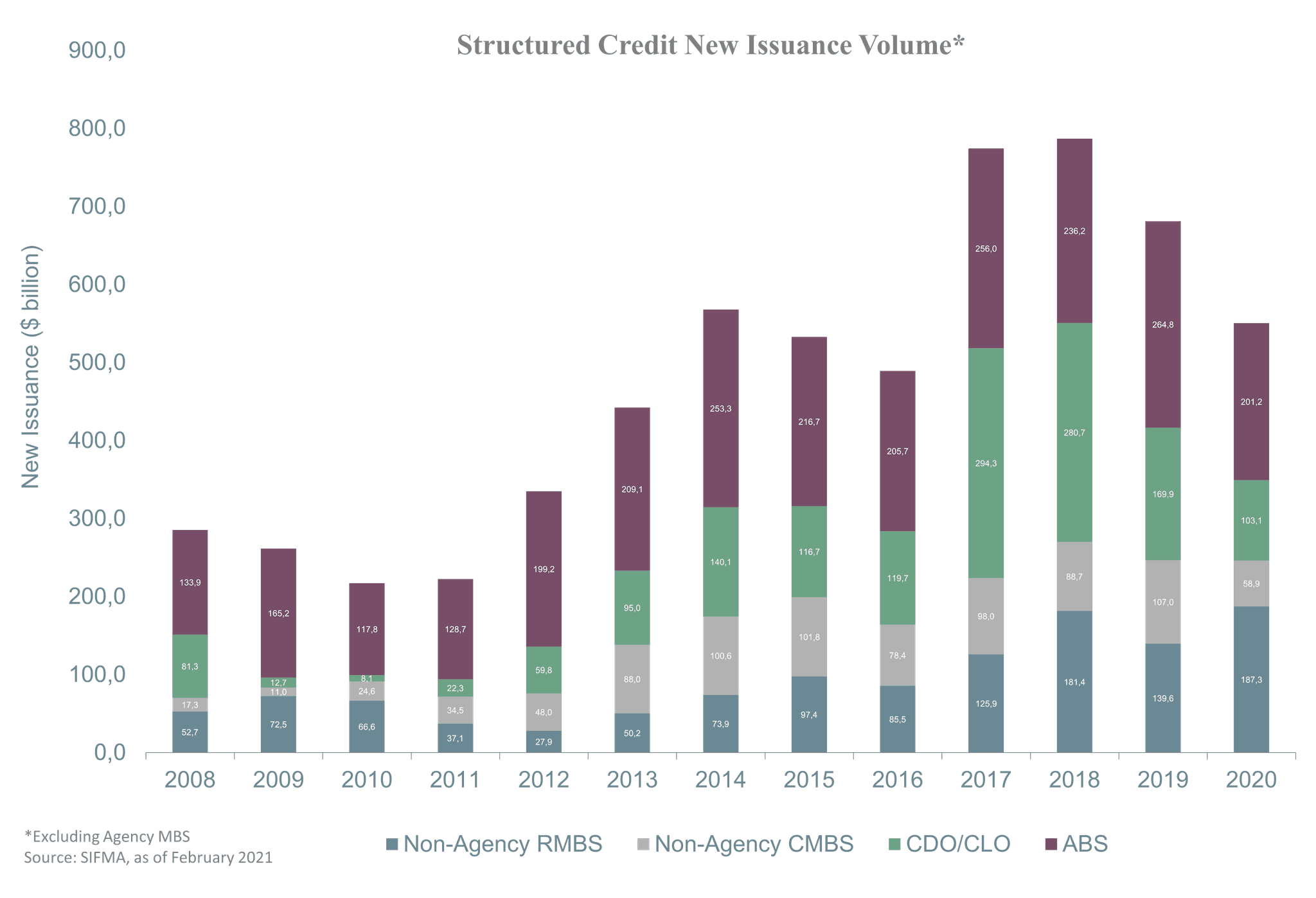

The new issuance market (not including agency MBS) has shown resilience throughout 2020. While YoY new issuance volume fell 19%, H2 2020 YoY new issuance volume was up 5%. The majority of the decline resulted from the market standstill throughout March to May, and the velocity of the rebound helped mitigate drawdowns even in weaker structures. When including agency MBS, YoY new issuance volume was up 8%.

Summary

Summary

Structured credit presents investors tailored, robust investment opportunities, which historically have been avoided due to the complexity surrounding them. The market today has proven its resilience through the COVID-19 crisis and has shown that sound fundamental changes took place in the industry following the 2008 fallout.

"In today’s low-yielding environment, structured credit offers an attractive income return profile versus comparable conventional fixed income assets, as average spreads across the tranches exceed those of investment grade and high yields bond."

Additionally, they have low interest rate and inflation sensitivity through their floating rate nature, and encompass diversification through the securitization of a pool of underlying assets.