Private Debt in an Institutional Portfolio

A more consistent income stream, attractive risk-adjusted returns, and diversification - these are among the benefits that attract institutional investors to allocate to private debt in their portfolio strategies.

Private Debt in an Institutional Portfolio

Ever since the global financial crisis in 2008, new banking regulations, such as Basel III, have curtailed banks' ability to lend. Consequently, private debt has emerged to replace this funding void, and S&P Global estimates that the asset class has grown tenfold to USD 412 billion over the past decade.

Today, we also find ourselves in a rising rates environment, which means traditional fixed income may no longer act as a ballast to equity in a portfolio. Given that private debt is not marked to market and is rates-proof with flexible rates, the asset class now plays a strategically important role in institutional investors' portfolios.

But how should institutions approach the allocation process to this asset class?

Private Debt Allocation Process

I. Strategy

The first step is the strategic process to determine the allocation level to private debt. There are three key considerations:

Given differing strategies and the illiquid nature of transactions, private debt does not have reliable and observable monthly return data to derive return patterns.

Due to private debt’s low volatility, investors need to decide whether to assess risk as the fundamental risk or the mark-to-market volatility.

It will take around two to four years to build up a robust private credit allocation.

II. Diversification

Next, the ideal diversification parameters need to be defined. Investors can diversify across the following factors:

Borrower type: Corporates vs real assets

Strategy: Senior secured lending, mezzanine lending, distressed lending, special situations

Geography: Global, North America, Europe, Asia

Managers: Optimal number of managers and different fundraising schedules

Time: Different vintage years

III. Cash Flow Planning

Different managers have different fundraising schedules and investment speed. Therefore, investors must consider how to plan or time future cash flows in order to maintain the target allocation level to private debt. In addition, effective cash flow planning allows diversification across vintage years and tilt to markets that may be more attractive at a given point in time.

IV. Due Diligence

Investors must carefully analyze whether a manager's results are consistent with the risk profile of the undertaken strategy. Crucial factors to look out for include the team's experience, competitive advantage, sourcing capabilities, credit underwriting skills, default protection and restructuring experience, loss rates, and recovery rates.

Selecting Private Debt Strategies

Private debt encompasses the following strategies:

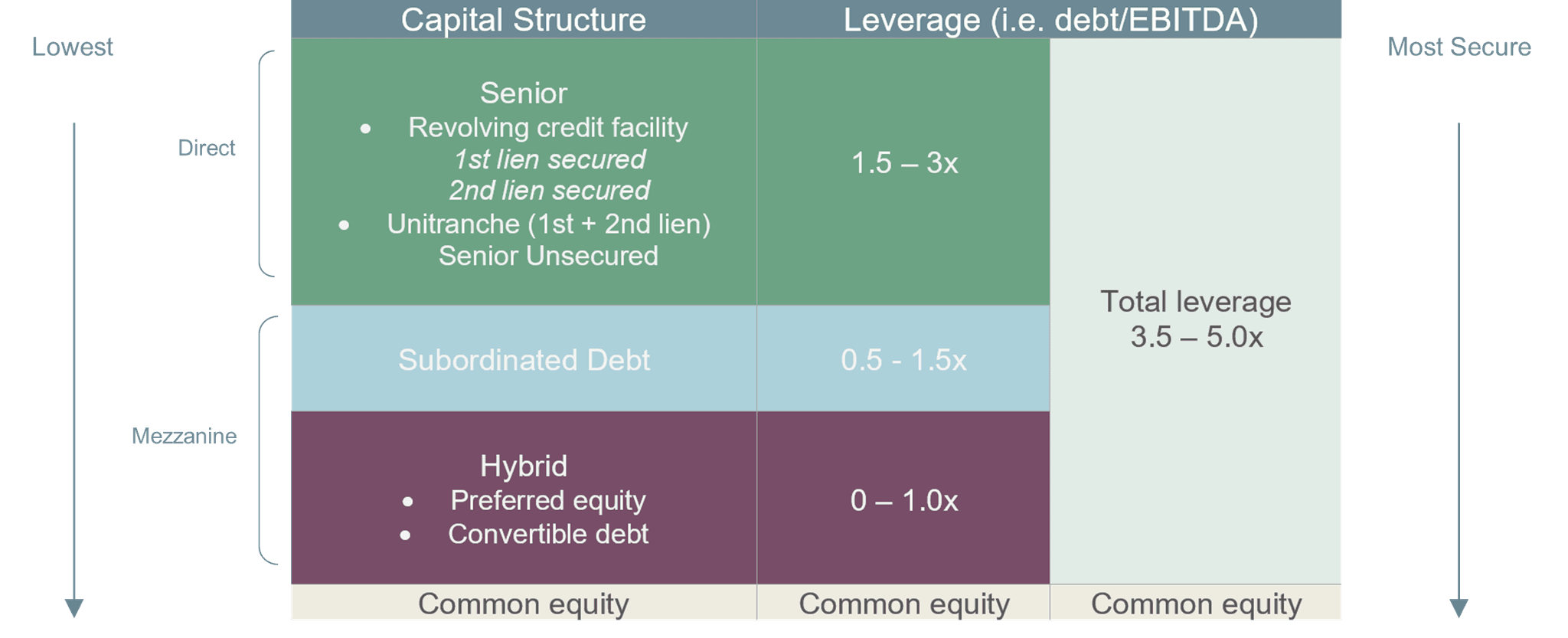

Direct lending - refers to non-bank lending to corporates. Loans can be 1st lien, 2nd lien, stretched senior, or unitranche (both 1st & 2nd lien). 1st lien loans are the most senior in the capital structure and the first to be paid back, as shown in the following chart. Direct lending is also typically secured and comes with debt covenants.

Mezzanine debt - debt that is subordinate to 1st and 2nd lien loans. These loans are typically unsecured but embedded with equity upside (e.g., warrants).

Distressed debt - refers to debt of stressed (e.g. spread of 600-800 bps above the risk-free rate) or distressed companies (e.g. spread of >1,000 bps). Strategies include trading (i.e. quick flips), non-control (influencing restructuring negotiations), and control (converting debt to equity control).

Special situations - are flexible capital solutions that do not fall strictly into any of the earlier strategies. Generally, special situation lending involves opportunistic credit with equity-linked upside when market liquidity is low, value is high, or in situations requiring highly specialized underwriting.

Niche strategies - examples include trade finance, royalties, aircraft leasing, etc.

Allocating to Private Debt Managers

According to Preqin, there are over 2,000 managers that have a private debt strategy today. So how should investors go about selecting a manager?

The private debt business is very relationship-driven. For managers that do sponsor deals (i.e., financing of private equity deals), a helpful indicator is the number of sponsor relationships and number of repeat sponsors relationships. Certain managers have a high number of repeat deals, and this often reflects their ability to execute a deal quickly, reliably, and flexibly. Managers that do non-sponsored deals tend to have specific industry expertise that places them ahead of the pack, such as in specialized sectors like healthcare.

Investors would want to allocate to managers who can add differentiated value. For instance, managers who act as lead lenders can add value in various ways, such as being able to control pricing, deal structure, and terms. Such managers typically receive higher deal fees and can better track a borrower’s operational and financial metrics. Lead lenders can also better control the workout process if a loan goes bad. Other ways of adding value include specializing in sectors, geographies, or niches (e.g. SMEs in the lower-middle market) that are less efficient or have the expertise to turn around a company if the loan starts to fail. Some managers also run highly diversified portfolios of loans that number in the hundreds.

What are a manager’s default, loss, and recovery rates? Numbers matter. These are important validations of whether a manager’s downside protection efforts are sufficient. Although it sounds perfect on paper to have a manager who has never had a default, it can be a potential weakness as they may not have the experience to deal with problem loans. Having a manager who has been through multiple cycles is also ideal.

Other questions to consider include: How fast does the portfolio ramp up and down, and what fees are charged? Are the fees charged on committed or invested capital? Are leveraged sleeves provided? How does the manager typically protect the downside and what is the LTV of the average deal?

Conclusion

While allocating to private debt in an institutional portfolio is not a complicated process, it is challenging to execute well. The industry moves at such a dynamic pace that it is difficult to keep up if one is not in the industry.

As part of Petiole's diversified private market investment programs, we have been harnessing private debt's potential over the past years. Reach out to us today to find out how to incorporate private debt into your investment strategy.