The COVID-19 dislocation has forced airlines to sell some of their crown jewels to create liquidity. The restricted new issuance in the debt market has created attractive repricing opportunities for lenders to top-tier credits and patient equity investors.

The Great Dislocation of 2020

The year 2020 has had an unprecedented impact on the aviation industry. Up to two-thirds of the world’s fleet was grounded in April as the pandemic spread across the globe, causing significant revenue declines which greatly increased the need for liquidity by airline operators. This global drive for capital caused indiscriminate repricing of aviation assets, leading to attractive investment opportunities.

The dislocation affected not only the prices of aircraft, but as a large percentage of lessees sought deferrals ranging from 3 to 12-months, it cascaded into a material decline in rent collections in the aircraft pooled asset-backed vehicles. The broader market selloff in structured products further affected the situation and as a result, aviation ABS debt sold off materially across senior and subordinated tranches. While the most senior tranche, known as Class A, has since recovered, the junior tranches, known as Class B and C, remain at depressed prices as the holders of the tranches were mostly levered up hedge funds while new buyers have been slow to step into this market segment. Investment banks have also become sellers of aircraft pooled asset-back vehicle debt, as they started taking mark-to-market losses in their aviation books and sought to de-risk.

The ABS new issuance space came to a complete halt due to COVID-19. Pent-up demand and record dry powder have allowed for the market to slowly re-open at favorable terms to junior tranche holders.

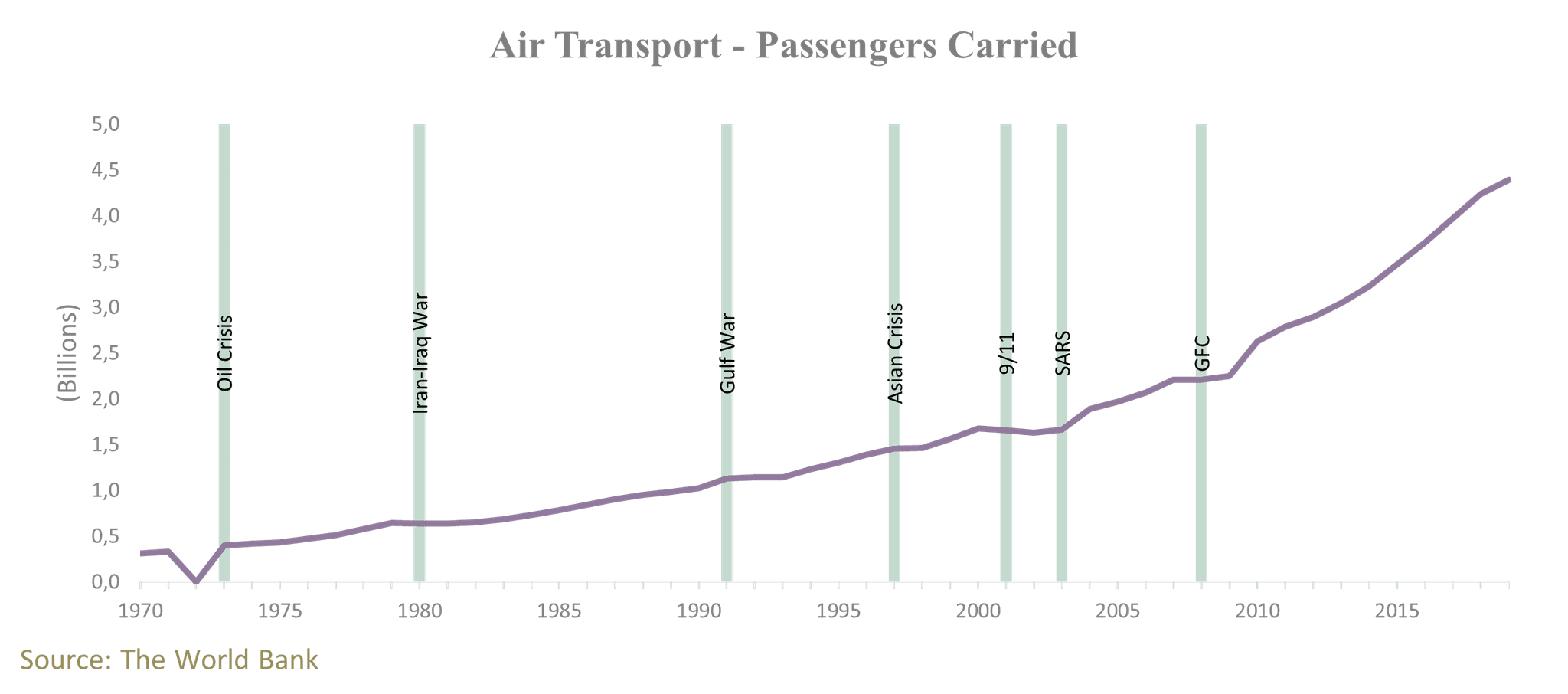

Aviation in Previous Crises

Despite numerous crises such as 9/11, the SARS epidemic and the GFC, the airline industry has doubled approximately every 15 years, in terms of passengers carried. The industry has on average taken only between 12-24 months to recover to pre-crisis levels before continuing its strong growth trajectory. The longest recovery on record was following 9/11, when systematic and behavioral changes took place. Since the GFC in 2009, though, the commercial airline industry has not only recovered but thrived. Prior to 2020, the industry’s fundamentals were improving at a greater rate than the broader global economy as globalization took hold and the emerging middle class globally found an increased need for mobility. According to IATA, passenger traffic has averaged an annual 6% growth since the GFC.

The recovery profile is expected to take place in 3 phases, with variation across geographies:

Phase 1: Domestic (increased focus on narrow-body aircraft)

Phase 2: Interregional (focus on both narrow-body and wide-body aircraft)

Phase 3: International (increased focus on wide-body aircraft)

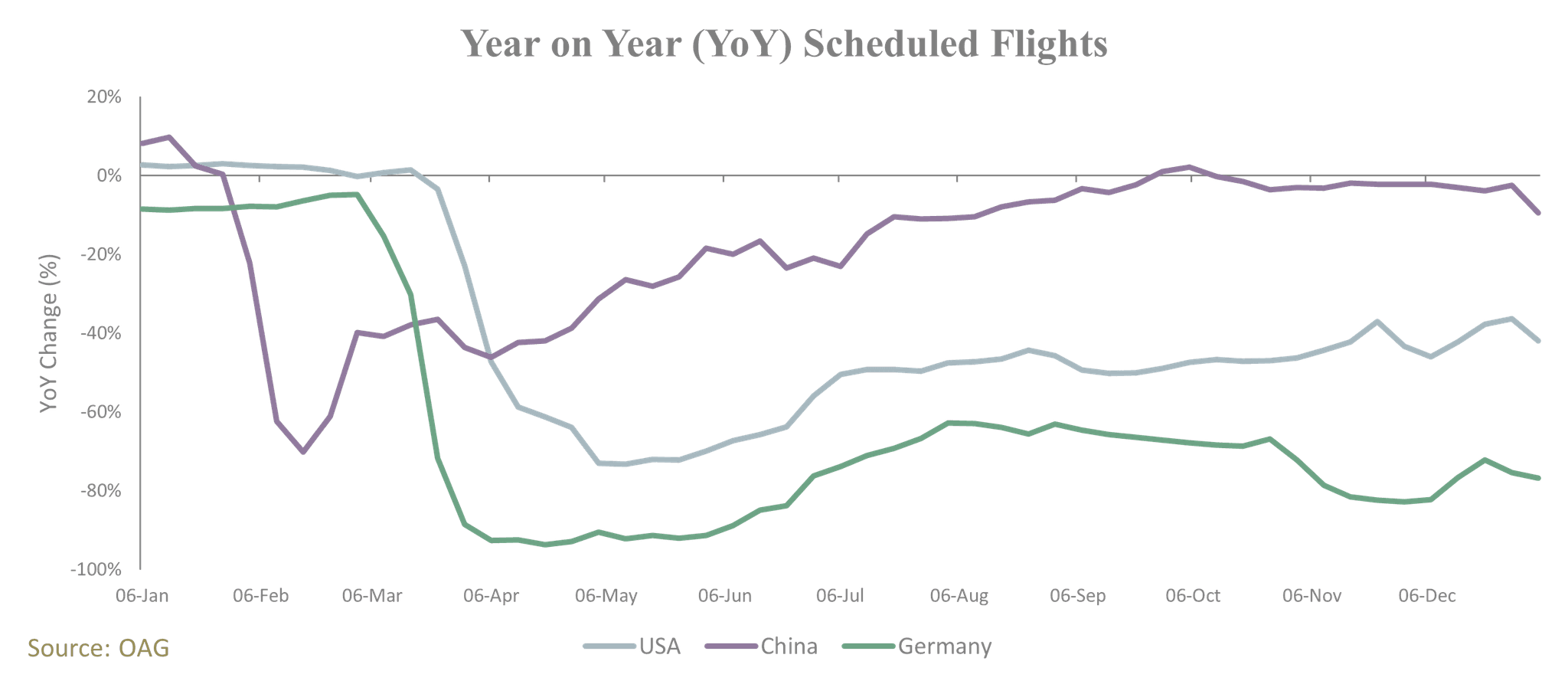

As of today, scheduled flights out of China are at 2019 levels YoY, and domestic load factors have exceeded 80%. International capacity utilization on the other hand is lagging at around 50%, expected to fully recover only in Phase 3.

IATA is predicting global revenue passenger kilometers (RPKs) to recover to pre-COVID-19 levels by 2024. However, as a result of the pandemic, a pendulum effect has occurred in the industry whereby manufacturers (predominantly Boeing and Airbus) are producing less aircraft, and aircraft operators are retiring aircraft at a higher rate. With this combined effect considered, the net supply of aircraft is expected to decline by 2024.

The recovery is being driven by strong government support globally totaling approximately US$160 billion, with government-owned and tier 1 carriers being the primary recipients. The U.S. government has provided the largest support with over US$80 billion alone, followed by Germany, France, and the Netherlands. Surprisingly, support within China has been quite muted, as its vaccine response and domestic market size counteracted declines in passenger revenues.

Alongside the attractive repricing that has taken place in the industry, this potential outcome is giving outsized return upside to investors in the space.

Investing Across the Capital Structure

Investing in the aviation space can be done both through equity (known as “hard metal”) and through debt (mainly in the form of securitizations). Equity generally comes either in the form of (a) direct aircraft purchases or (b) sales leasebacks, where airlines sell their aircraft and then immediately lease them back from buyers. Investments on the debt side are more nuanced, but also offer attractive opportunities:

Export Credit Agency (ECA) Debt. Credits guaranteed by an ECA; these are set on standardized terms, with a maximum tenure of 12 years

Unsecured Bonds. Publicly issued bonds not collateralized by underlying assets; more popular with leasing companies who prefer flexibility in term and payment profile

Secured Loans. Private loans collateralized on underlying aircraft equipment

Asset-backed Securities (ABS). Structured products favored by airline leasing companies; the leasing company acts as the servicer to the portfolio (i.e. dealing with maintenance, repossession and sale of aircraft)

Enhanced Equipment Trust Certificate (EETC). Structured debt instruments issued by a single airline; similar to ABS, notes (which include coupon and principal repayments), EETCs are issued to investors in tranches. EETCs typically provide credit enhancement to that of the underlying issuer as a result of tranching the notes, use of a liquidity facilities and cross-default provisions across the underlying collateral.

Further categorizations come within the aircraft themselves where commercial aircraft are typically divided into four categories: narrow-body, wide-body, regional jets, and turboprops. In general, aircraft have economic lives of 20-25 years, with cargo aircraft having longer lives at around 35 years due to fewer daily cycles than passenger aircraft. Lastly, the aircraft market is divided into four life segments: new, younger mid-life, older mid-life, and end-of-life.

Conclusion

The dislocation in the aviation industry experienced in 2020 was the largest in history, creating an excellent window for investment opportunities. Government support has been larger and faster than ever before, and yet despite these interventions, attractive pricing remains available to investors.

Consequently, Petiole will be taking advantage of this significant dislocation by partnering with the best managers in the industry that have demonstrated the ability to construct diversified portfolios of the highest quality airline credits, and with the experience to identify the best relative value assets within both debt and equity.