Private Credit: Income Repositioned for a New Market Cycle

Income has once again become central to portfolio construction. What has changed is how that income is sourced.

The traditional 60/40 portfolio, long viewed as a dependable framework for balancing growth and stability, has faced increasing strain. Public fixed income, historically perceived as defensive and predictable, has demonstrated greater sensitivity to inflation dynamics, policy shifts, and interest rate volatility.[1] While headline yields may appear compelling, duration risk and price fluctuations have reduced the consistency many investors once relied upon.

Within this environment, private credit has evolved from a peripheral allocation into a structural component of modern portfolios. What was previously considered a specialist segment now plays a critical role in financing the real economy. Looking ahead, private credit is no longer simply a yield enhancer. It reflects a broader transformation in how businesses access capital.

At Petiole, we view this evolution as enduring rather than cyclical.

The Structural Pullback of Traditional Lenders

For decades, banks were the primary lenders to mid-sized companies. That landscape has shifted meaningfully.

Following the global financial crisis, regulatory reforms strengthened banking resilience through higher capital requirements and stricter oversight. These reforms enhanced systemic stability, yet they also constrained banks’ capacity and appetite for certain types of corporate lending, particularly in the middle market where transactions are often bespoke and balance-sheet intensive.[2]

As a result, many fundamentally sound companies have encountered tighter access to traditional bank financing.

Private credit providers have stepped into this space. Rather than displacing banks outright, they have increasingly served segments banks have deprioritized. Private lenders offer structured, customized financing solutions to companies seeking execution certainty, flexibility, and long-term capital partnerships.

Importantly, this is not a temporary substitution effect. As regulatory frameworks remain firmly in place, private lenders are becoming a lasting pillar within corporate capital formation.

Structural Yield with Embedded Protection

Private credit’s growing appeal is closely linked to how returns are structured and safeguarded.

A large portion of private credit strategies focuses on senior secured lending. These instruments occupy the highest priority within a company’s capital structure and are typically backed by collateral. In scenarios of financial stress, senior lenders stand first in line for repayment.

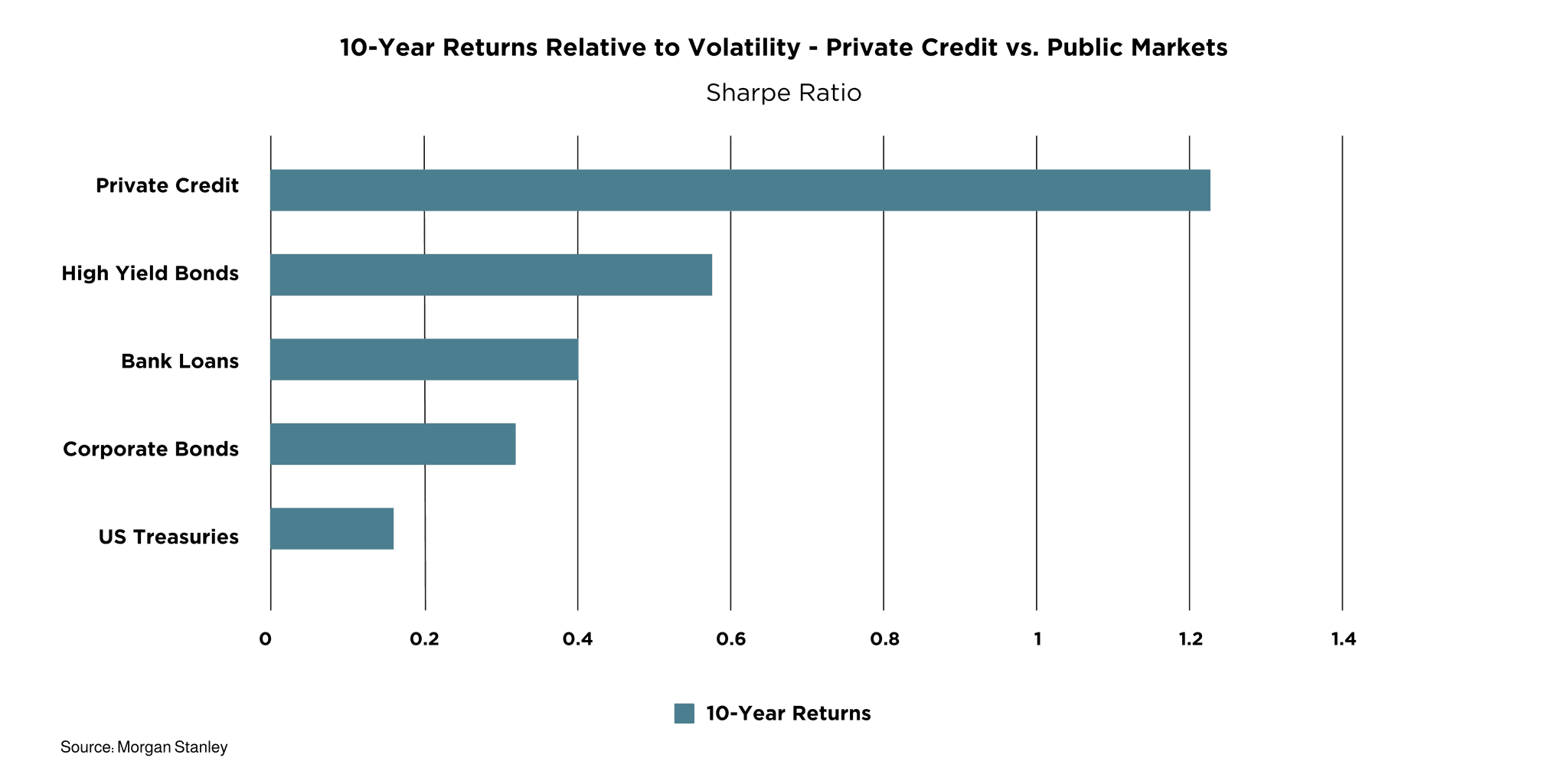

In addition, many private loans are structured with floating rates. Income therefore adjusts alongside changes in benchmark interest rates, reducing the duration sensitivity commonly associated with traditional bonds. Even as rates moderate from recent peaks, private credit continues to benefit from an illiquidity premium and contractual income streams that often remain comparatively attractive relative to public fixed income markets.

According to Morgan Stanley, global private credit assets under management surpassed $3 trillion in 2024, rising from approximately $1 trillion a decade earlier, with continued expansion expected in the years ahead.[3]

The combination of senior positioning, collateral protection, and floating-rate income has positioned private credit as a compelling solution for investors seeking income without assuming full equity risk exposure.

Managing Risk in Uneven Conditions

Private credit is frequently described as resilient. That resilience does not stem from an absence of risk, but from the structure of risk management.

Unlike public bond markets, private lending operates through direct relationships. Loan agreements commonly include financial covenants, reporting obligations, and ongoing engagement between lenders and borrowers. This structure allows issues to be identified earlier and, when appropriate, addressed in coordination with management teams.[4]

Defaults can occur in any credit environment. However, senior secured positioning and active portfolio oversight have historically supported more favorable recovery outcomes compared to unsecured or covenant-light credit structures.

As the current market cycle progresses, default rates in private credit are expected to normalize gradually amid uneven economic conditions across sectors and geographies.[5] Even so, forward expectations suggest defaults are likely to remain below long-term historical averages.[6]

In this setting, dispersion is likely to widen. Differences in underwriting standards, structuring discipline, sector exposure, and portfolio construction will increasingly influence outcomes. The framework within which capital is deployed therefore becomes critical.

The Importance of Access and Manager Selection

Despite its scale, private credit remains relationship-driven and less accessible than public markets.

Many high-quality lending opportunities are sourced through established networks and longstanding institutional relationships. Manager capability, borrower quality, downside protection, and structuring expertise can vary materially. As a result, return dispersion across managers can be significant.

For investors, diversification across borrowers, industries, and credit strategies remains essential. Equally important is disciplined manager selection grounded in underwriting rigor and structural safeguards.

At Petiole, private credit is integrated within a broader portfolio context. As an asset manager and investment manager, Petiole focuses on partnering with established credit managers and sourcing institutional-quality opportunities characterized by disciplined underwriting, structural protection, and thoughtful portfolio construction. The objective is not simply to enhance yield, but to pursue income generation with consistency across market environments.

Income in a Structurally Changing Landscape

Income continues to play a foundational role in portfolio construction. Public fixed income remains relevant, yet its behavior during periods of volatility has become less predictable.

Private credit offers an alternative framework. Income is typically supported by contractual cash flows and senior positioning, while the asset class’s sustained growth reflects lasting shifts in corporate financing rather than short-term market dislocations.

This is less about forecasting the direction of interest rates and more about aligning portfolios with the way capital formation now operates.

In a more complex investment environment, private credit has become an integral component of modern asset allocation. Through disciplined selection and structured access, Petiole integrates private credit into diversified portfolios with a focus on structural income and prudent risk management.