Since October 2020, U.S. bank stocks have climbed an astounding 90%, well ahead of the 42% gain in the S&P 500. But is there any further upside for the sector?

In October 2020, Petiole Asset Management published an article about their extremely bullish position on U.S. banks. Drago Kolev, a Portfolio Manager at Petiole called it, “the best opportunity in decades to invest in the U.S. banking sector.”

Q: Drago Kolev, you have had a stellar track record over the past 11 years as a Portfolio Manager. What did you see last year that gave you conviction to buy U.S. bank stocks?

We saw the pandemic as a natural disaster. With the unprecedented U.S. government response, we told our clients that the COVID-19 downturn would not be a repeat of the 2008-2009 Global Financial Crisis (the ‘GFC’). Instead, the economic shock more closely resembled Hurricane Katrina’s impact on New Orleans. Following Katrina, the city’s economy was wiped out. However, banks were not overburdened with bad loans thanks to quick government intervention. Last year, we believed the recovery in the U.S. would be like Katrina for the same reason. We were right. U.S. GDP dropped by roughly $2 trillion during the pandemic but was met with more than $5 trillion in stimulus. It didn’t appear to be a catastrophe.

Banks also entered the pandemic with double the capital they did before the GFC – the most in 80 years. Together with the stimulus, it was clear banks would only experience 1-2% systemwide loan losses at most. Once the market realized this and vaccines were introduced, banks rallied strongly in early 2021.

Q: Has your view changed?

Despite 90% appreciation in large regional banks since the COVID-19 bottom, we continue to own them in our liquid funds as we expect further upside from here.

I noticed that in this century, each time the Fed raised rates three times or more in a single year, U.S. banks have climbed above 2.25x price-to-tangible book value. The current forecast implies three increases in the Federal Funds Rate in 2023. Bank stocks will need to rise 30% from current valuations in order to re-rate to 2.25x.

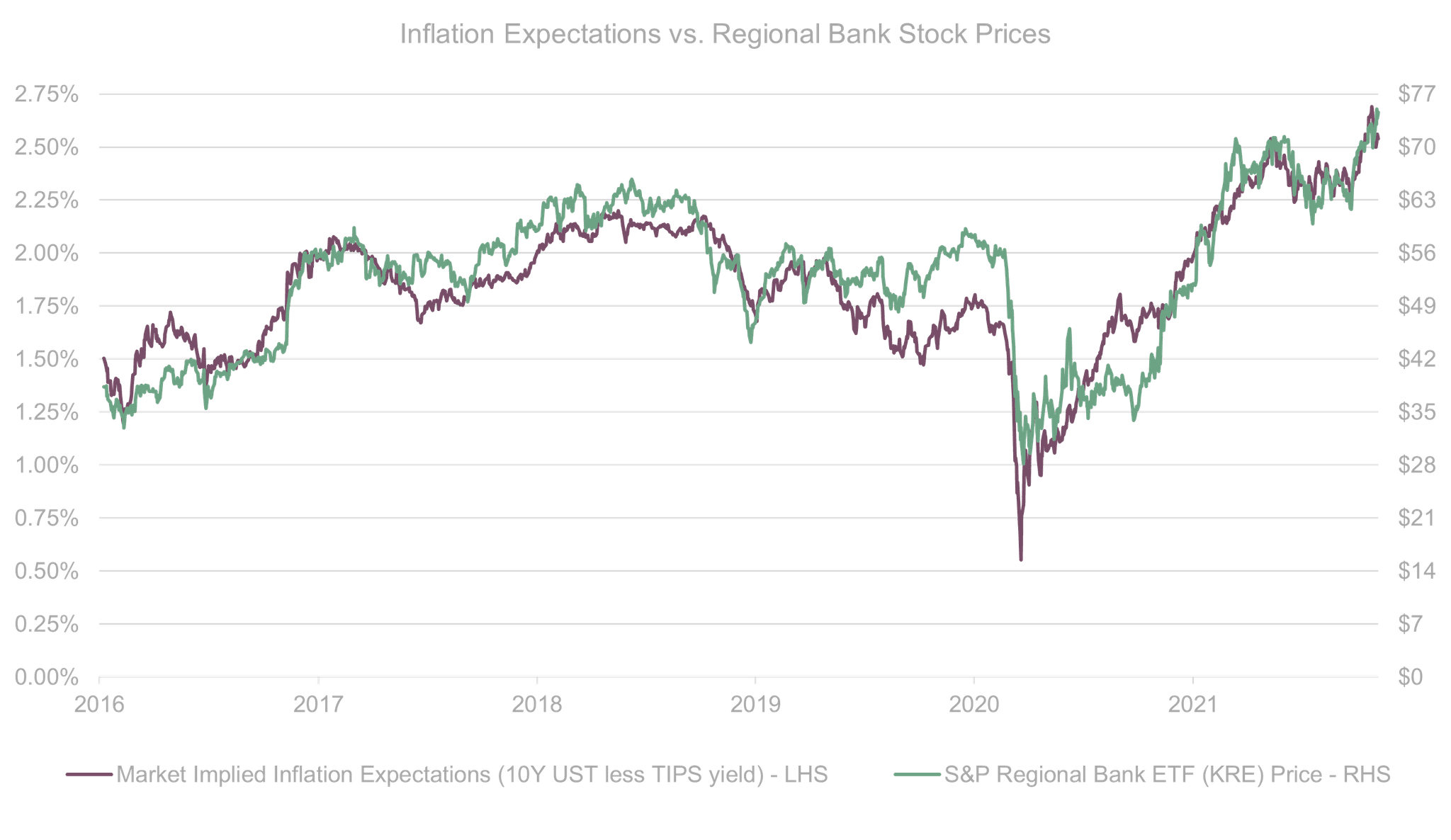

A Fed tightening signals a robust economic recovery with rising inflation, which would benefit banks. The graph below shows that the price of regional bank stocks has closely followed inflation over the past years. Bank stocks are a great inflation hedge, and the market expectations for future inflation are currently pointing north.

Q: So, what are community banks?

The US banking system today is still rather fragmented, with roughly 4,800 community banks each holding less than $10 billion in assets. Of these, around 700 are listed or traded over-the-counter and present a very compelling investment opportunity following the COVID-19 disruption.

Community banks proved irreplaceable during the pandemic. Even though they only held 15% of total U.S. banking assets, they made 60% of the most crucial first round of government-sponsored business (Paycheck Protection Program, or PPP) loans.

While larger regional peers rose from 1x to 1.8x price-to-tangible book value over the past year, community banks are still stuck trading at roughly 1x.

Q: Why are community banks so cheap?

At the start of a cycle, investment capital is channeled to larger banks as institutions seek to ‘buy the sector.’ Consequently, the smaller names fall behind. We saw this pattern unfold after the 2016 presidential election. But market forces closed the gap over time, and community banks even outperformed larger names.

Another factor is the June 2021 annual Russell 2000 Index rebalancing, when a record 79 banks were dropped from the index. These deletions resulted in heavily discounted bank stocks. However, these valuations tend to recover following the rebalancing.

We plan to use the same playbook here. We doubt that the market will let community banks trade at 1x price-to-tangible book value for much longer. They should close the gap with larger regional peers thanks to interest rate hikes and M&A activity. Because we believe the U.S. bank sector multiple is going to 2.25x or higher, the upside in community banks could be well over 100%. We are accumulating a portfolio of smaller banks as we believe their valuations are likely to double in the next three years.

Any last words?

If you feel regretful about missing the rally from last year, buying small U.S. banks could be a superb opportunity to catch up.